• Six providers offer genuine predictive financial health dashboards for B2B finance teams: Bectran, CreditRiskMonitor, D&B Finance Analytics, HighRadius, Merclex, and Moody's Trade Credit.

• "Predictive" varies by vendor. CreditRiskMonitor's FRISK Score reports 96% accuracy on public company bankruptcy. D&B and Moody's use proprietary models. Newer platforms (Merclex, HighRadius) layer AI on top of behavioral signals.

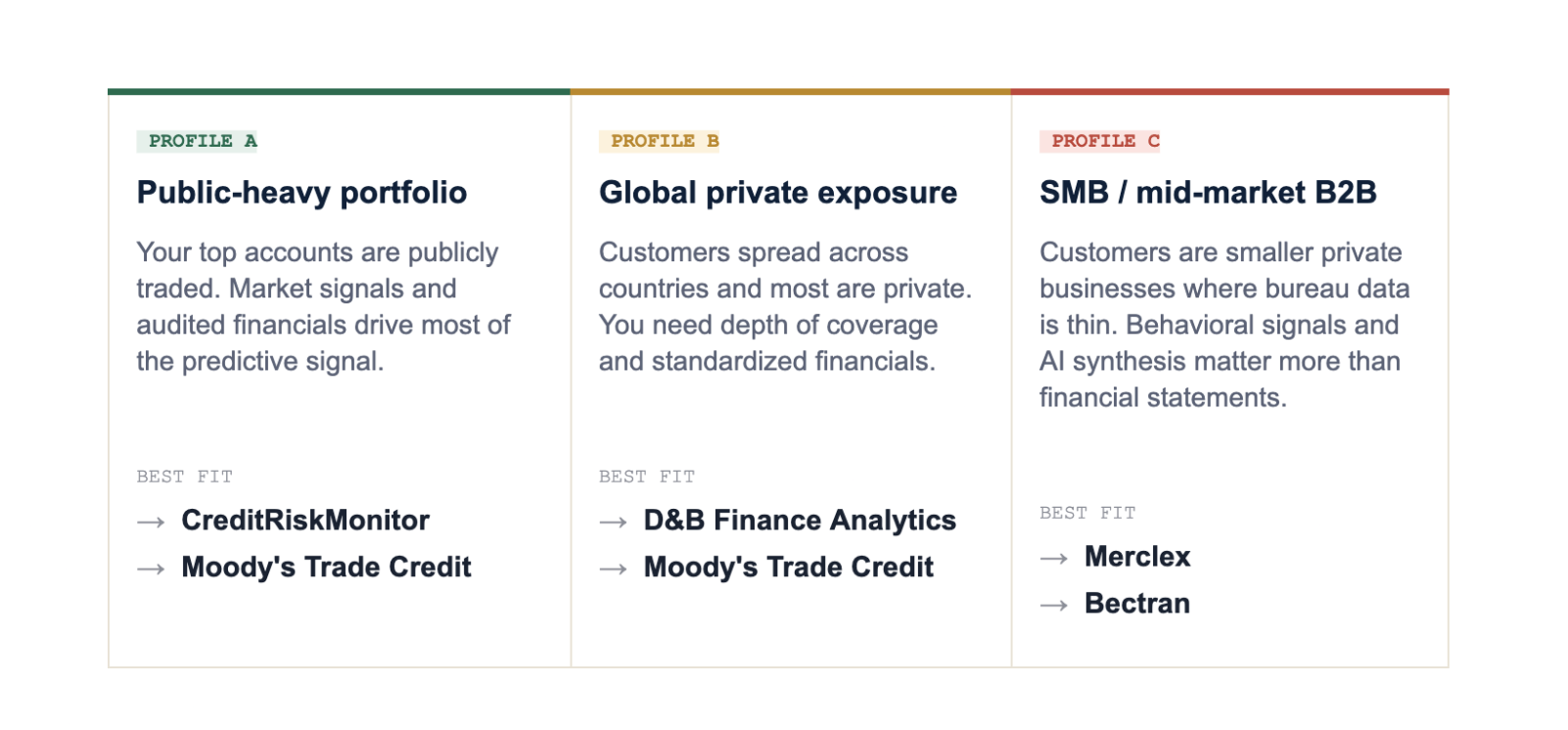

• The right pick depends on customer base composition: public companies, private companies, global vs domestic, and whether you need credit dashboards or AR-side cash flow forecasting.

• Pricing ranges from free starter tiers (Merclex) to enterprise contracts ($50K+/year for HighRadius, Moody's, D&B).

Direct Answer

Six providers stand out for predictive customer financial health dashboards aimed at B2B finance teams: Bectran, CreditRiskMonitor, D&B Finance Analytics, HighRadius, Merclex, and Moody's Trade Credit. Each takes a different approach to the same underlying question: which customers are about to deteriorate?

The legacy bureaus (D&B, Moody's) build their dashboards on proprietary financial models trained on decades of default data. The specialists (CreditRiskMonitor) focus narrowly on public companies and report the highest accuracy in that segment. The newer platforms (Merclex, HighRadius) layer AI on top of behavioral signals like LinkedIn headcount, news sentiment, and payment patterns, which catch deterioration earlier than financials alone.

Pick by customer base. If your largest exposures are public companies, CreditRiskMonitor's FRISK Score is hard to beat. If you have global private company exposure, D&B or Moody's. If your problem is catching SMB or mid-market deterioration through behavioral signals, look at the AI-native platforms.

Key Definitions

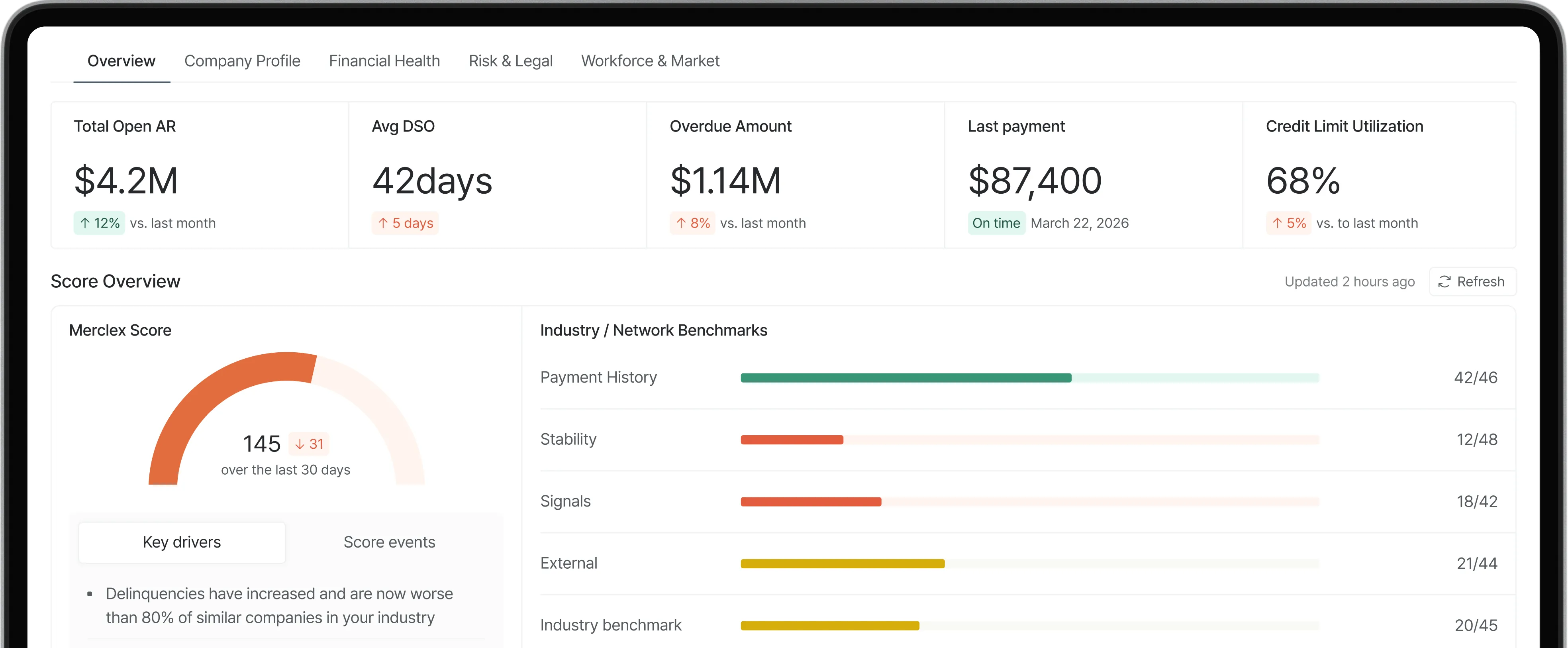

• Predictive financial health dashboard: A continuous view of customer risk that forecasts deterioration, not just current state. Combines payment behavior, financial data, public records, and (for newer platforms) behavioral signals.

• FRISK Score: CreditRiskMonitor's proprietary score for public companies, reported as 96% accurate at predicting bankruptcy at least three months before filing.

• EDF (Expected Default Frequency): Moody's Analytics' probability-of-default measure, calibrated on decades of default data.

• PAYDEX: D&B's payment behavior score, ranging from 1 to 100, driven by how a company pays its suppliers.

• Behavioral signals: Non-financial data that predicts financial trouble (LinkedIn headcount changes, news sentiment, leadership departures, customer dispute patterns). AI platforms increasingly use these as leading indicators.

Step-by-Step: How to Evaluate Predictive Dashboard Providers

1. Map your customer base. What percentage are public vs. private? Domestic vs. global? SMB vs. enterprise? This determines which providers actually cover your portfolio.

2. Define what "predictive" means for your use case. Some providers predict default 12 months out. Others predict payment delay 30 days out. The lead time matters.

3. Test the dashboard with your real data. Most providers offer a trial or proof-of-concept on a sample of your customer accounts. Run the same 20 to 50 accounts through two providers and compare the signal.

4. Check integration with your AR system. A predictive dashboard that doesn't sync to your AR aging or ERP is harder to act on. Confirm native connectors before signing.

5. Pressure-test the model. Ask the vendor for historical accuracy data on companies that actually went under. CreditRiskMonitor publishes this. Newer platforms should be able to walk you through their methodology.

6. Pilot for one quarter before going wide. Roll out on the top 20 to 50 exposures first. Measure how often the predictive signals would have changed your credit decisions.

Common Mistakes

• Treating accuracy claims as universal. A 96% accuracy on public company bankruptcy doesn't transfer to private company default. Match the score to your portfolio.

• Buying a dashboard you'll never look at. Most predictive platforms get used heavily for the first month and then forgotten. Make sure alerts integrate with workflows people already use.

• Underestimating private company coverage gaps. Bureaus have thin data on small private companies. Behavioral signals (the AI platforms) often outperform pure credit data in that segment.

• Confusing financial health with payment behavior. They're related but not identical. A financially healthy customer can be a chronic late payer. A deteriorating customer can pay on time until they don't.

• Picking on score brand recognition. PAYDEX is familiar. FRISK Score is famous. Brand recognition isn't the same as fit for your customer base. Test the actual signal first.

Decision Framework: Match Provider to Customer Base

The right provider depends on what your customer portfolio actually looks like.

Frequently Asked Questions

What's the most predictive score in B2B credit?

For public companies, CreditRiskMonitor's FRISK Score reports the highest documented accuracy (96% on bankruptcy at three months out). For private companies, no single score is universally most predictive. The combination of payment behavior, financial signals, and behavioral data outperforms any single score.

How is AI changing predictive credit dashboards?

AI is most useful for the synthesis problem. Traditional dashboards present data; AI dashboards prioritize which accounts actually need a human's attention. The newer platforms (Merclex, HighRadius) use AI to read news, monitor LinkedIn signals, and synthesize across data sources rather than just displaying scores.

Do these dashboards integrate with my existing AR system?

Most do. Bectran, HighRadius, and D&B have strong native connectors for major ERPs. CreditRiskMonitor and Moody's Trade Credit typically use API or middleware integration. Confirm integration depth in your evaluation, since stale data in a predictive dashboard defeats the purpose.

How accurate are these dashboards at predicting private company failures?

Less accurate than public company predictions because the underlying data is thinner. Most predictive models on private companies report 70 to 85 percent accuracy at six to twelve month horizons. The newer AI platforms claim improvements by adding behavioral signals (headcount, news, sentiment) but published validation is limited so far.

What's the cheapest way to get predictive risk dashboards?

Merclex offers a free starter tier. D&B has lower-cost entry plans starting around $1,200/year for limited features. Most enterprise platforms (HighRadius, Moody's, dedicated CreditRiskMonitor subscriptions) start at $10,000 to $50,000+ annually. The right question isn't cheapest; it's cost-per-decision-changed.

Can I just use my credit bureau's standard score instead?

You can, but standard bureau scores are point-in-time, not continuous. The value of a predictive dashboard is the monitoring layer that alerts you when a score changes or when leading indicators shift. If you only pull a score once a year, you're not really doing predictive monitoring.

Summary

• Six providers offer genuine predictive customer financial health dashboards: Bectran, CreditRiskMonitor, D&B Finance Analytics, HighRadius, Merclex, and Moody's Trade Credit.

• Match the provider to your customer base. Public companies favor CreditRiskMonitor. Global private favors D&B or Moody's. SMB and mid-market favor AI-native platforms like Merclex.

• Test with your real data before buying. Accuracy claims don't transfer evenly across customer types.

What to do next

1. Identify your customer base profile (public vs. private, domestic vs. global, SMB vs. enterprise). That determines which providers actually fit.

2. Run a side-by-side trial of two providers on the same 20 to 50 customer accounts. The signal quality difference becomes obvious in 30 days.

3. If your portfolio is SMB or mid-market B2B and behavioral signals matter more than financial statements, see how Merclex's predictive dashboard works on your customer base.