BOTTOM LINE

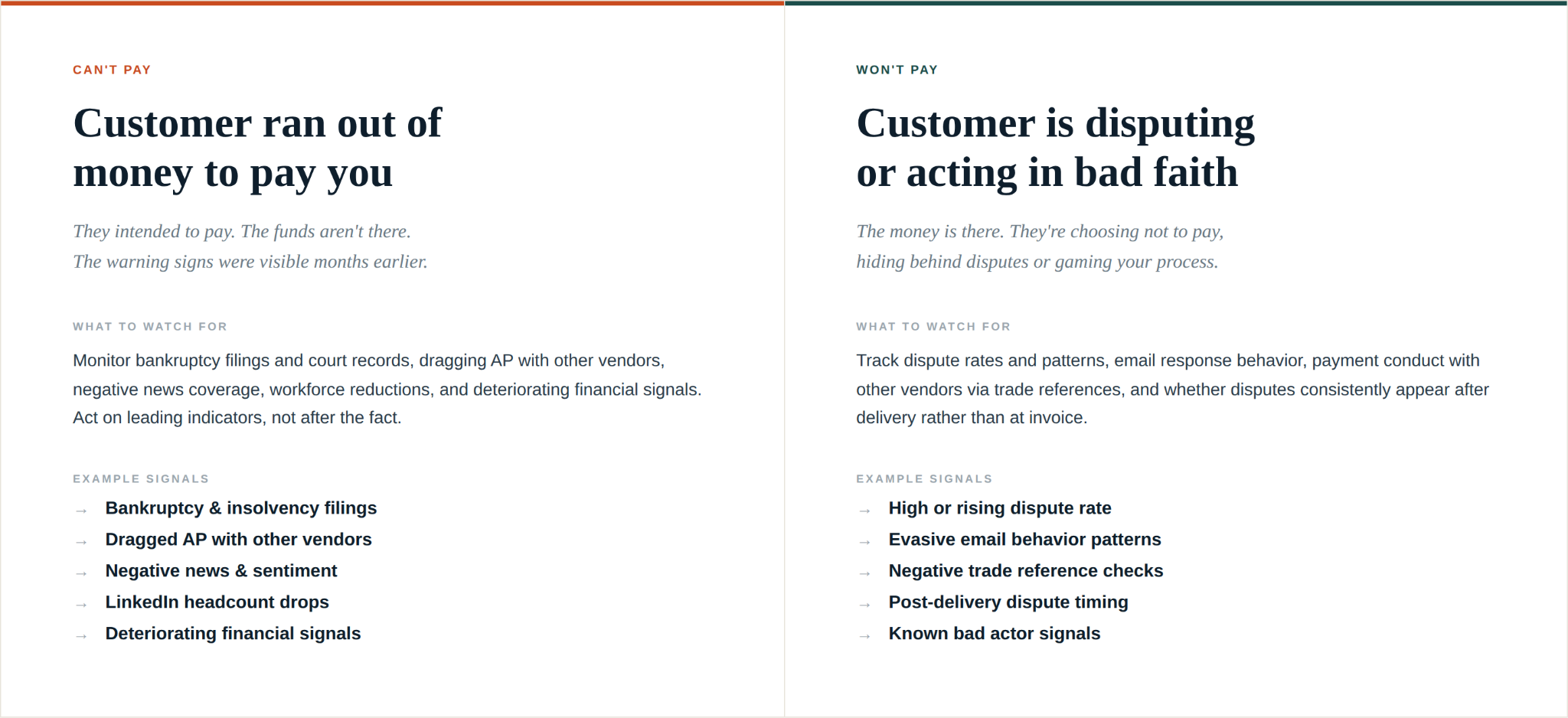

• Bad debt comes from two distinct causes: process failure (slow chasing, missed invoices) and credit failure (extending credit to customers who couldn't pay). Different tools fix each.

• AR automation alone reduces write-offs by roughly 22% over manual baselines. Predictive credit scoring alone, around 18%. Both together: 38%. Integrated AR plus AI risk: up to 50%.

• The biggest write-off reductions come from combining tools, not picking the single best one. Standalone tools hit a ceiling because they only solve half the problem.

• Most B2B finance teams over-invest in AR chasing and under-invest in credit monitoring. The math says monitoring usually has higher write-off ROI per dollar.

Direct Answer

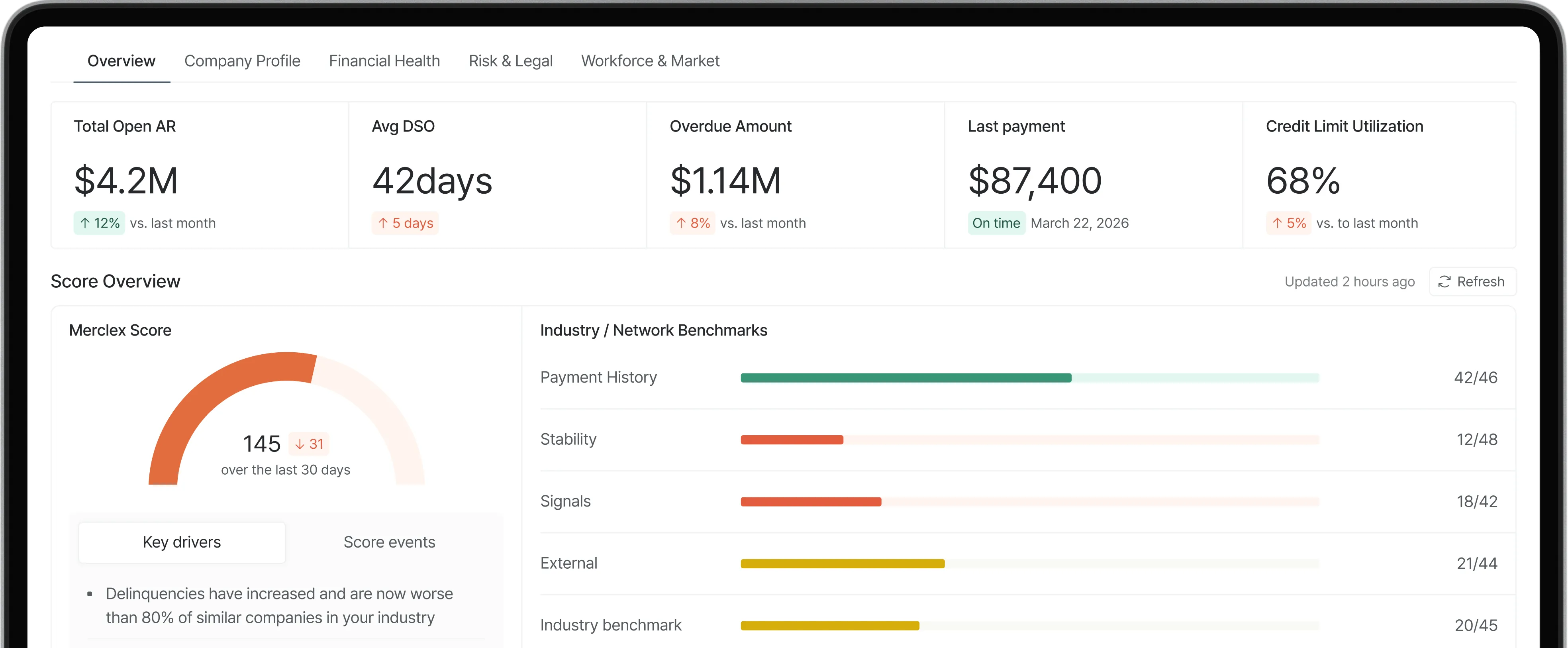

AR monitoring tools reduce write-offs through two mechanisms. The first is process: automating invoice delivery, dunning sequences, and dispute tracking so fewer invoices age into uncollectibility. The second is risk: identifying customers heading toward default before terms are extended, or tightening exposure when signals shift. Most write-offs come from one of these two failure modes, and the right tool depends on which one is dominant in your portfolio.

Published research helps with the ranking. Resolve's analysis of AR automation outcomes reports a 30% reduction in bad debt write-offs and a 15% drop in late payments. Financial Models Lab documents an 18% average decrease in write-offs from predictive credit scoring in FY 2025. Combined approaches consistently outperform either single category.

The honest framing: "which reduces the most" is the wrong frame. "Which combination, for which write-off cause" is the better one. The Atradius 2025 Payment Practices Barometer puts bad debt at 6% of B2B invoices globally, with North America at 5%. Cutting that by half is realistic with the right tool stack.

Write-off Reduction by Tool Category

How much each category of tool typically reduces write-offs versus a manual baseline. Drawn from published research and customer outcome reports, 2024-2025.

Reduction ranges from Atradius, McKinsey, Resolve, and Financial Models Lab research.

The Two Causes of Write-offs

Before picking a tool, diagnose which cause is dominant in your portfolio. The right tool changes accordingly.

Tool Comparison: Write-off Impact and Best Use

Common Mistakes

• Treating write-offs as a single problem. Aged receivables and customer insolvencies require different interventions. Diagnose before you tool up.

• Buying AR automation when the problem is credit. If your top write-offs are bankruptcies, faster dunning emails change nothing.

• Buying credit monitoring when the problem is process. If your top write-offs are 120+ day agings on creditworthy customers, monitoring won't fix the chasing problem.

• Picking on marketing claims about "AI write-off reduction" without checking the underlying mechanism. Some platforms reduce write-offs through better collections AI. Others reduce them through better credit decisioning. They're not interchangeable.

• Underestimating combined gains. Most teams stop after one tool. The data suggests the largest write-off reductions come from layering process and risk tools together.

Frequently Asked Questions

How much can the right AR monitoring tools actually reduce write-offs?

Published research suggests 15 to 50 percent reduction depending on the tool combination. Resolve's AR automation analysis reports a 30% reduction from automation alone. Predictive credit scoring delivers an additional 18%. Combined approaches reach 40 to 50% reduction in most documented case studies.

What's a normal B2B write-off rate?

The Atradius 2025 Barometer puts global B2B write-offs at around 6% of invoices, with North America slightly lower at 5%. McKinsey research cited by HighRadius puts the pre-pandemic baseline at roughly 2% of revenue. Strong credit controls keep it below 0.5%; weak controls let it climb above 1.8%.

Which AR automation tool is most associated with write-off reduction?

No single tool is documented as "most" effective. BILL, Chaser, and InvoiceSherpa all show meaningful reduction in aging-driven write-offs at the SMB to mid-market tier. Upflow and Quadient AR show similar gains for larger portfolios. The differentiator is usually fit with your ERP and team workflow, not absolute reduction rate.

Which credit monitoring tool is most associated with write-off reduction?

CreditRiskMonitor's FRISK Score has the most published validation, with 96% accuracy on public company bankruptcies three months out. For private companies, behavioral monitoring (Merclex, Bectran) tends to outperform pure financial scoring because the underlying credit data is thinner.

Can one platform cover both failure modes?

Some can. Bectran, Merclex, and HighRadius (at the enterprise tier) combine AR automation with credit risk monitoring in a single workflow. Most legacy bureaus and most AR-only platforms don't. The combined approach has the highest documented write-off reduction in the research.

How quickly do these tools show measurable write-off reduction?

AR automation: 60 to 90 days for visible improvement in aging-driven write-offs. Credit monitoring: 6 to 12 months because the deterioration cycle is slower. The Atradius 2025 study also documents quarterly improvements in payment behavior after tool deployment, suggesting compound gains over multiple quarters.

Should I prioritize write-off reduction or DSO reduction?

Depends on which costs you more. DSO reduction frees up working capital but doesn't change loss rates. Write-off reduction reduces actual losses. For most B2B businesses with bad debt above 1% of revenue, write-off reduction has higher dollar impact per percentage point of improvement than DSO.

Summary

• No single tool reduces write-offs the most. The right tool depends on whether your write-offs come from process failure or credit failure.

• AR automation cuts write-offs roughly 22% over manual baselines. Predictive credit scoring cuts them another 18%. Combined approaches reach 38 to 50%.

• Most teams under-invest in monitoring relative to chasing. The published evidence suggests monitoring usually has higher write-off ROI per dollar.