- The earliest signals are payment behavior changes (Days Beyond Terms creeping up), workforce contractions on LinkedIn, and shifts in how a customer talks about money.

- Public records (UCC filings, lawsuits, tax liens) confirm trouble. They don't predict it.

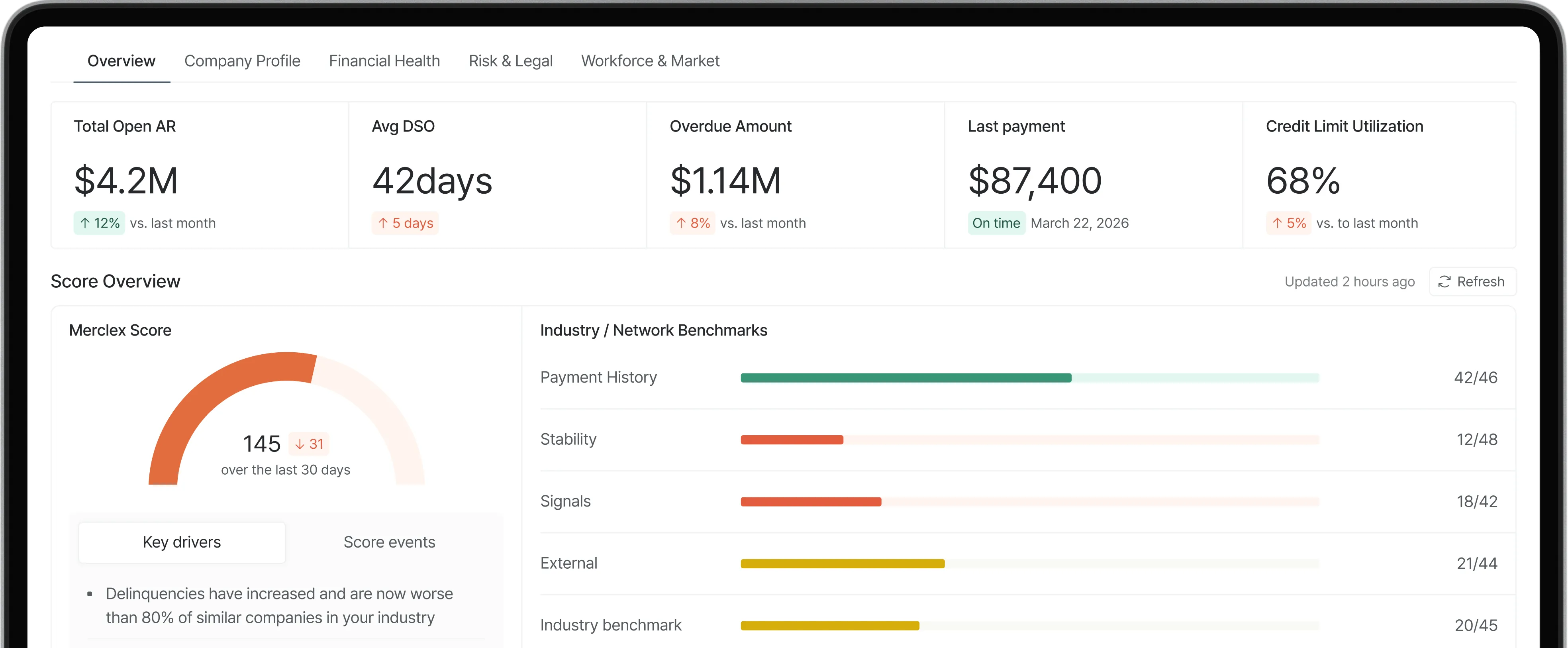

- Watching credit scores is the most common mistake. Scores update months after behavior already shifted.

Direct Answer

A business customer in real trouble usually shows it in three places before a credit bureau catches on: how they pay, who works there, and how they talk to you about money.

The earliest signal is almost always payment behavior. Not a single late payment, but a pattern. Days Beyond Terms drift higher. Partial payments replace full ones. The customer who used to pay net-30 starts paying net-50, with explanations that sound thinner each time. By the time a credit score reflects what's happening, you're already 2 to 4 months behind.

The second tier is workforce signals. A 10% LinkedIn headcount drop in 60 days is hard data, especially when finance or operations leadership is leaving. Public records (UCC filings, lawsuits, tax liens) come third. They confirm what payment behavior should have already told you.

Quick Comparison: Signal Types and Lead Time

Key Definitions

- Days Beyond Terms (DBT): Average days a customer pays past stated terms. The most actionable single number in trade credit risk.

- UCC filing: A public notice when a creditor takes a secured interest in a debtor's assets. Searchable through state Secretary of State databases.

- Going concern qualification: An auditor's note expressing doubt about a company's ability to operate the next 12 months. Found in 10-K and 10-Q filings on SEC EDGAR.

- Leading vs. lagging indicators: Leading indicators predict trouble (payment drift, headcount, sentiment). Lagging indicators confirm it (credit downgrades, bankruptcy filings).

Step-by-Step: How to Spot a Failing Customer

- Pull 12 months of AR aging. Calculate DBT per customer. Flag accounts where DBT increased by 5+ days month over month for three consecutive months.

- Check UCC filings on top 20 exposures. Most state Secretary of State sites are free. New blanket liens in the last 90 days are a real signal.

- Run news sentiment on the same 20. Search the company name plus "layoffs," "lawsuit," "restructuring," or "default."

- Pull LinkedIn headcount trends. Drops over 10% in 60 days warrant a closer look. Leadership departures warrant immediate attention.

- Have a real conversation. Here's the part people skip: call the controller at any account with two or more signals. How they handle the call tells you a lot.

Common Mistakes

- Watching scores instead of behavior. Scores are designed to be stable. Behavior moves first.

- Treating public records as primary signals. They're confirmations, not predictions.

- Reviewing the portfolio quarterly. Quarterly cadence misses most failures.

- Treating one signal as enough. One signal is noise. Two or three together are when you act.

Decision Framework: The 3-2-1 Rule

A signal counts if any are true: DBT up 10+ days from baseline, UCC filing in last 90 days, lawsuit or tax lien filed, LinkedIn headcount drop of 10%+ in 60 days, negative news, going concern note, customer requesting term extensions, or two or more contact changes in 90 days.

FAQ

What's the single most reliable signal a customer is going under? A sustained increase in Days Beyond Terms combined with a story that keeps changing. Either alone is noise. Together they're the most consistent leading indicator across industries.

How early can these signals be detected? Behavioral and workforce signals typically appear 6 to 12 months before bankruptcy. Public records appear 3 to 6 months before. Credit score changes happen within 3 months of default.

Is LinkedIn headcount data actually reliable? Yes, with caveats. It's most reliable for companies above 50 employees. The signal is strongest when paired with which roles are leaving. Finance, operations, and senior leadership departures matter more than uniform reductions.

How do I monitor private companies without a credit bureau subscription? A lot is free. UCC filings through Secretary of State sites. Federal court lawsuits through CourtListener. News and LinkedIn are public. The gap is trade payment data, which usually requires a subscription or a tool like Merclex that aggregates these signals.

What does it mean when other vendors cut credit terms with my customer? It usually means they've seen the same patterns you should be looking at. If three other vendors have shortened terms in the last quarter, treat that as a signal. Trade payment exchanges (D&B's, Experian's) capture this.

Should I rely on a single credit score or use multiple? Use multiple. D&B's PAYDEX is trade-payment driven. Experian's Intelliscore pulls more financial data. CreditRiskMonitor's FRISK Score adds market signals (96% accurate for public company bankruptcy, per their research). Disagreements between scores are themselves useful data.

Summary

- Watch behavior, not scores. Payment patterns lead bureau updates by months.

- Layer your signals. One is noise, two warrant attention, three or more demand action.

- Continuous monitoring beats periodic review. Customers who fail rarely give 30 days notice.

What to do next

- Run the watchlist exercise on your current AR aging this week. Flag accounts with rising DBT for three consecutive months.

- Check UCC filings and recent news on your top 20 exposures.

- If you're managing 50+ active customers, look at continuous monitoring tools like Merclex alongside your bureau data.