• A credit report is a snapshot. Continuous monitoring is a feed. They answer different questions.

• Reports are best for one-time decisions: onboarding, credit limit reviews, dispute resolution. Monitoring is best for ongoing portfolio risk.

• Most credit teams over-rely on reports and under-invest in monitoring, which is why customers go under without warning.

• The right setup uses both: a report to make the decision, monitoring to know when the decision needs to be revisited.

Direct Answer

A credit report is a snapshot taken at a moment in time. Continuous monitoring is a feed of changes happening across a customer's business in real time. Both are useful, but they answer different questions.

A credit report tells you what a company looked like when the report was generated: payment history, public records, financial statements, credit score. It's a static document. By the time you read it, the underlying data is days or weeks old. Reports are designed for decisions: should we onboard this customer, what credit limit makes sense, do we extend net-30 or net-60.

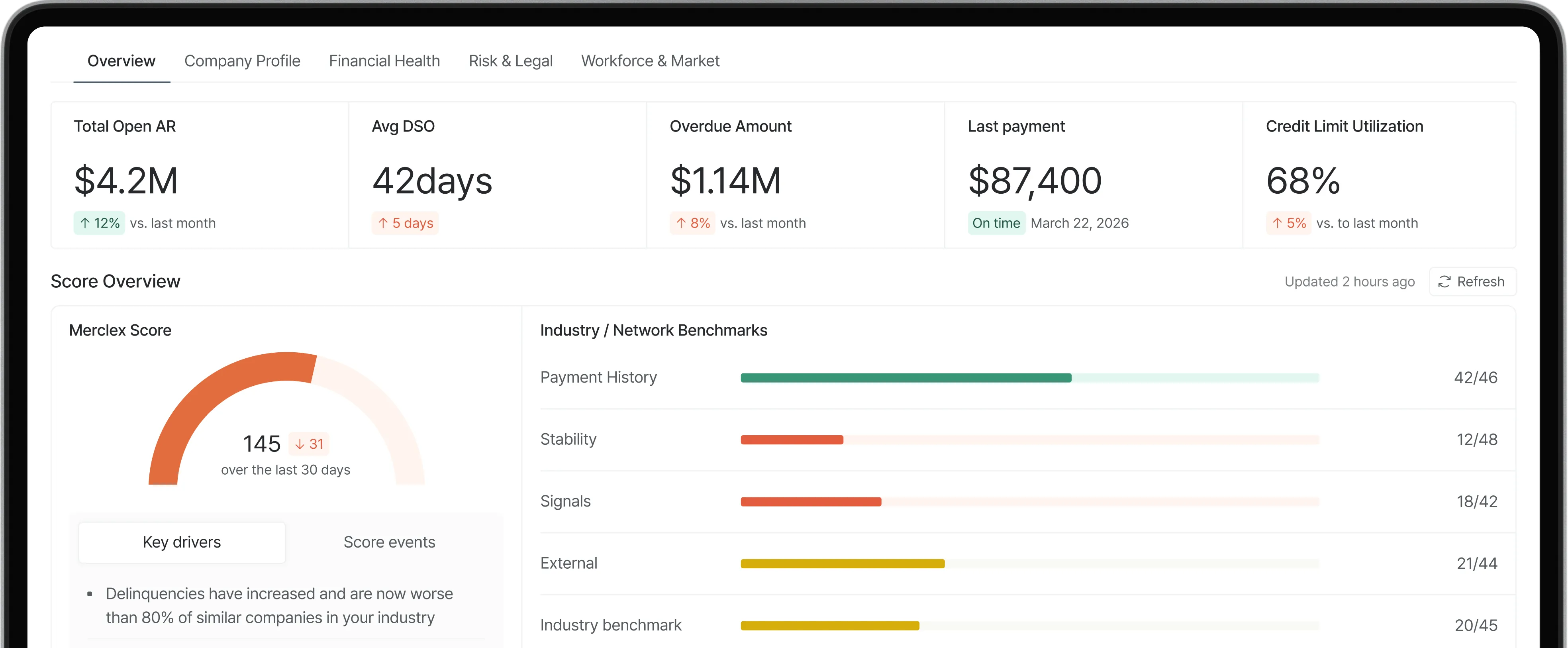

Continuous monitoring tracks the same kinds of signals reports cover, plus signals reports never include (LinkedIn headcount, news sentiment, earnings call language, leadership departures, executive sentiment). Instead of generating a document on demand, monitoring pushes alerts when something material changes. It's designed for awareness: which of my 200 active customers shifted overnight.

The honest answer to which is better is neither. They serve different purposes and most B2B credit teams need both.

Quick Comparison: Reports vs. Continuous Monitoring

DIMENSION

CREDIT REPORT

CONTINUOUS MONITORING

Frequency

Pulled on demand or annually

Tracks continuously, alerts in real time

Output

Static document, snapshot

Stream of signals and alerts

Lag time

Days to weeks behind reality

Hours to days behind reality

Best use

Decisions: onboarding, limits

Awareness: changes after onboarding

Cost model

Per-report or subscription

Subscription, scales with portfolio

Action trigger

Manual review and decision

Push notification with context

Coverage gap

Stale by the time you read it

Misses things never made public

Key Definitions

• Credit report: A document compiled by a bureau (D&B, Experian, Equifax, Creditsafe) summarizing a company's payment behavior, public records, financial profile, and credit score at a point in time.

• Continuous monitoring: Ongoing surveillance of a customer's risk signals across data sources, with automated alerts when changes occur. Includes both traditional credit data and behavioral signals like LinkedIn headcount and news sentiment.

• Trade payment exchange: A reciprocal program where suppliers report customer payment behavior in exchange for visibility into how that customer pays others. The data feeds both reports and monitoring.

• Leading vs. lagging signals: Leading signals (payment drift, headcount changes, news sentiment) appear early. Lagging signals (UCC filings, lawsuits, credit downgrades) confirm trouble that already exists.

Step-by-Step: How to Combine Both Effectively

1. Pull a fresh credit report at onboarding. This is your decision document. It establishes the baseline for credit limit, terms, and any guarantees you require.

2. Set up continuous monitoring on every approved customer. The cost per account is small. The upside is catching change before it becomes a problem.

3. Define what triggers a fresh report. Monitoring alerts of material change (DBT increase, news event, headcount drop) should trigger a new report, not just a note.

4. Schedule formal credit reviews using reports. Annual reviews on top exposures, semi-annual or quarterly on highest-exposure customers. Use the report to make decisions, not the monitoring feed.

5. Feed monitoring data into collections. When an account hits monitoring thresholds, AR teams should know before they make the next collection call. Context changes how you collect.

Common Mistakes

• Treating a report as ongoing protection. A report from six months ago tells you nothing about what's happening today. Many credit teams pull a report at onboarding and never refresh it.

• Buying monitoring without acting on alerts. Monitoring only matters if alerts route to a human who has authority to act. Otherwise it's expensive noise.

• Assuming the same vendor does both well. Most bureaus offer both products, but they're often built by different teams with different update cadences. Evaluate the monitoring product on its own merits.

• Ignoring private companies because reports are weak there. For private B2B customers, monitoring (LinkedIn, news, payment behavior) often produces better signal than the underlying credit report.

• Pulling reports too often instead of monitoring. Pulling a report monthly costs more and tells you less than continuous monitoring with quarterly report refreshes.

Frequently Asked Questions

Are credit reports still useful in 2026?

Yes. Reports remain the best format for one-time decisions: onboarding a new customer, setting an initial credit limit, defending a credit decision in a dispute. The structured format is what makes them useful. The mistake is treating them as ongoing protection.

Can continuous monitoring replace credit reports entirely?

Not for most B2B credit teams. Reports are still the standard format auditors, lenders, and credit committees expect for decision documentation. Monitoring complements reports, but doesn't replace the legal and procedural role they play.

What signals does monitoring catch that reports miss?

LinkedIn headcount changes, news sentiment shifts, earnings call language, leadership departures, customer complaint patterns, social mentions. These signals often appear 3 to 9 months before they show up in a credit report or score.

How often should I pull a fresh credit report?

Annually as a baseline for active customers. More frequently when monitoring flags material change, or when you're considering a credit limit increase. Quarterly for top exposures regardless of monitoring.

Which is more expensive, reports or monitoring?

Depends on portfolio size. For small portfolios (under 50 customers), pulling reports as needed is usually cheaper. For larger portfolios, continuous monitoring is more cost-effective per account, because you're paying once for ongoing coverage rather than per-event for snapshots.

Do bureaus like D&B and Experian offer both products?

Yes. D&B sells both Finance Analytics (reports) and continuous monitoring add-ons. Experian and Equifax do the same. The quality of monitoring varies. Newer specialized platforms (CreditRiskMonitor for public companies, Merclex for B2B trade) often have stronger monitoring capabilities than the legacy bureaus.

Summary

• Reports are snapshots for decisions. Monitoring is a feed for awareness. They serve different purposes.

• Most B2B credit teams need both: reports at onboarding and review, monitoring everywhere in between.

• Monitoring catches signals reports never include, like headcount drops and news sentiment, often months before they show up in a credit score.