• Five platforms offer real B2B credit risk capabilities under $500 a month: D&B Credit Reporter, Experian Business CreditScore Pro, Merclex, Nav Business, and Bectran's entry tiers.

• "Credit risk software" is different from "AR automation." These tools assess and monitor the creditworthiness of your customers; they don't chase invoices.

• Most enterprise credit risk platforms (HighRadius, Moody's, full D&B Finance Analytics) start at $1,000+/month and don't fit this tier.

• Under $500/month works for SMB and lower mid-market teams managing fewer than 200 active credit relationships. Larger portfolios usually need enterprise pricing.

Direct Answer

Five platforms genuinely fit B2B credit risk software under $500 a month: D&B Credit Reporter, Experian Business CreditScore Pro (from $124/month), Merclex (free starter), Nav Business (from $50/month), and Bectran's lower-tier plans.

The category is narrower than buyers often expect. Most platforms marketed as "credit risk software" are enterprise tools with $10,000 to $100,000+ annual contracts, including HighRadius, full D&B Finance Analytics, Moody's Trade Credit, and CreditRiskMonitor. Those are built for finance teams of 10+ at companies with 500+ active credit relationships.

Under $500/month is the SMB and lower mid-market tier. You get core credit risk capabilities (credit reports, basic monitoring, alerts on score changes) but not the full enterprise feature set (custom scoring models, multi-currency, deep ERP integration, dedicated analyst support).

Key Definitions

• Credit risk software: Tools used by B2B sellers to assess and monitor the creditworthiness of their customers. Outputs include credit reports, risk scores, monitoring alerts, and decision recommendations.

• AR automation: Different category. Tools that handle invoice delivery, reminders, late fees, and collections after a credit decision has been made.

• Tradeline data: Records of how a company has paid its suppliers and creditors. The most actionable input for credit scoring.

• Continuous monitoring: A subscription that tracks changes in a customer's credit profile and alerts you when something material shifts (score changes, new lawsuits, payment behavior drift).

• DUNS Number: Dun & Bradstreet's unique business identifier. The standard reference for B2B credit data globally.

The Five Platforms in Detail

Listed alphabetically. Pricing reflects publicly available plans as of May 2026.

Bectran From $200/mo

Best for mid-market distributors that want credit risk and AR workflow in one platform.

Bectran is a B2B credit and order-to-cash platform with composite risk scoring, AI-driven fraud detection, and automated credit application workflows. Pricing is configuration-dependent and not publicly listed. Entry tiers typically fit under $500/month for limited seat counts; full deployments at larger companies run higher. Strong for distributors, building materials, and steel/metals sectors where they have deep customer references.

D&B Credit Reporter From ~$100/mo

Best for quick, on-demand reports on US private companies.

D&B Credit Reporter (different from the full D&B Finance Analytics platform) is the lighter-weight option for getting individual credit reports without an enterprise contract. Plans start around $99-$200/month for limited monthly report pulls. Reports include the PAYDEX Score and basic firmographic data. Useful for occasional credit checks, less useful for continuous portfolio monitoring.

Experian Business CreditScore Pro $124/mo

Best for detailed US tradeline data when report volume is moderate.

$1,495/year for 30 reports per month. The Intelliscore Plus score is widely accepted by SBA lenders, banks, and vendor credit programs. Add-on charges apply: $15 per report for trade payment detail, UCC filings, or inquiry data. Strong tradeline data, but the recently launched BusinessIQ 2.0 interface still trails newer SaaS platforms.

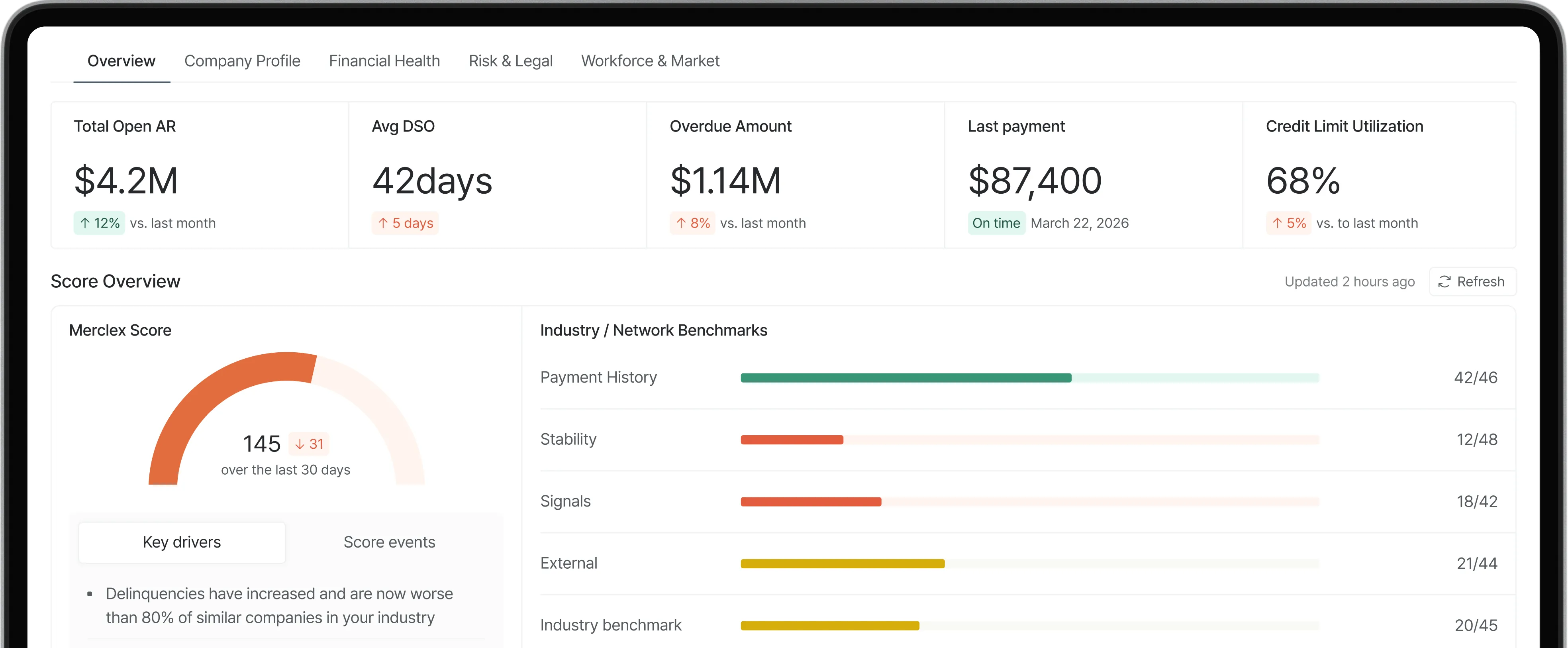

Merclex Free starter

Best for B2B trade businesses that want AI-driven credit monitoring with a modern interface.

Merclex combines credit onboarding (lawsuits, liens, judgments, fraud checks) with continuous AI monitoring of customer health signals (LinkedIn headcount, news sentiment, earnings, leadership changes). The free starter tier is genuinely usable; paid tiers are contact-for-pricing and positioned to compete with the legacy bureaus rather than the enterprise platforms. Strongest fit when behavioral signals matter more than deep traditional credit data.

Nav Business $50 to $150/mo

Best for small businesses focused on basic credit monitoring.

Nav's primary product is for businesses monitoring their own credit, but their business credit data is also available for B2B use cases. Less feature-rich than the bureau platforms but more affordable. The clean interface and SMB focus make it accessible for very small finance teams. Limited for portfolios above 30-40 active customers.

Common Mistakes

• Confusing credit risk software with AR automation. They solve different problems. AR automation chases invoices; credit risk software decides whether to extend credit in the first place.

• Picking on data brand recognition alone. D&B and Experian are familiar names, but their entry tiers are often more expensive than newer platforms with comparable signal quality for SMB use cases.

• Ignoring portfolio size. Under $500/month works well for portfolios under 200 active credit relationships. Larger portfolios need enterprise tiers or face cost-per-account that quickly exceeds enterprise pricing.

• Underestimating the difference between reports and monitoring. A platform that gives you one-time reports is fundamentally different from one that continuously monitors. Confirm before buying.

• Skipping the free tiers. Merclex and Nav both have free or freemium options. Use them to test data quality before committing to a paid plan.

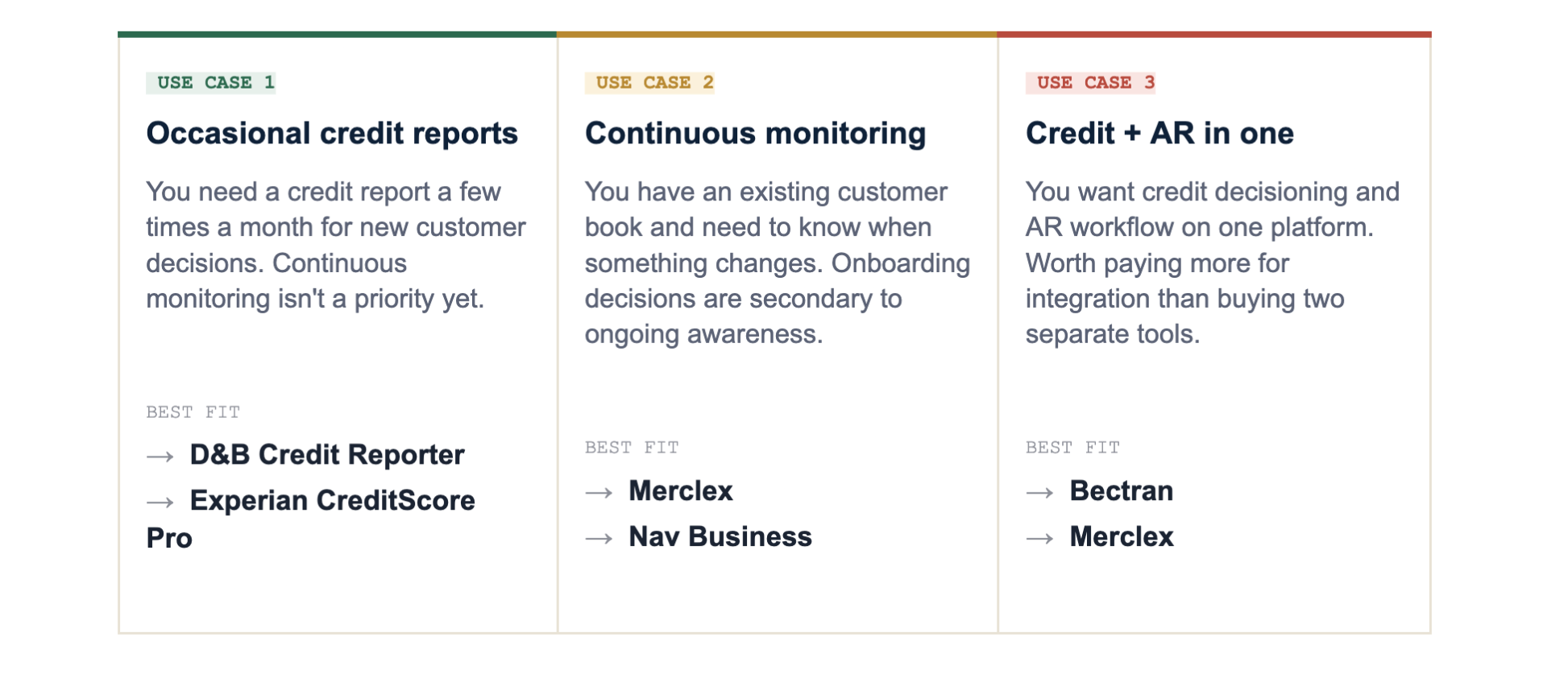

Decision Framework: Match Platform to Use Case

The right platform depends on what you actually need: quick reports, continuous monitoring, or full credit + AR workflow.

Frequently Asked Questions

Is $500/month enough for real B2B credit risk software?

For SMBs and lower mid-market teams, yes. Under $500/month covers basic credit reports, monitoring, and alerts on score changes. Enterprise features (custom scoring models, multi-currency, dedicated analyst support, deep ERP integration) typically require $1,000+/month.

What's the difference between credit risk software and AR automation?

Credit risk software assesses whether a customer should be extended credit and monitors their ongoing risk. AR automation handles invoice delivery, reminders, and collections after credit has been extended. Most teams need both; some platforms (Bectran, Merclex) combine the two.

Can I get B2B credit data for free?

Partially. Some basic business credit information is available through Nav, Tillful (now part of Nav), and free tiers from various platforms. Merclex offers a free starter tier with monitoring capabilities. Detailed credit reports and continuous monitoring of multiple companies almost always require a paid subscription.

Do these platforms integrate with my ERP?

Varies. Bectran has strong ERP integration for distributors. The bureaus (D&B, Experian) typically offer API access at their entry tiers but full integration may require upgrading. Merclex offers integrations with major accounting software (QuickBooks, Xero) at all tiers. Confirm specific connectors during evaluation.

Which platform has the most accurate credit data?

There's no single most accurate platform; it depends on your customer base. D&B has the broadest international coverage. Experian has the strongest US tradeline depth. AI-driven platforms (Merclex) add behavioral signals that none of the bureaus include. Most credit teams find that combining bureau data with behavioral signals produces the strongest overall accuracy.

Summary

• Five platforms genuinely fit B2B credit risk software under $500/month: Bectran, D&B Credit Reporter, Experian Business CreditScore Pro, Merclex, and Nav Business.

• Pick by use case: occasional reports, continuous monitoring, or credit + AR combined. Price is the constraint; use case is the deciding factor.

• Free starter tiers (Merclex, Nav) let you test data quality without commitment. Use them before buying.

What to do next

1. Identify your primary need: credit decisions, ongoing monitoring, or both. Don't buy a continuous monitoring subscription if you only need occasional reports.

2. Test two platforms on the same 10 to 20 customer accounts. Signal quality differences become obvious within a month.

3. If your customer base benefits from behavioral signals beyond traditional credit data, see how Merclex's free starter compares on your actual portfolio.