• Lowering DSO is rarely about chasing harder. It's about better decisions at the front of the cycle (credit screening, terms) and consistent execution at the back (automation, monitoring).

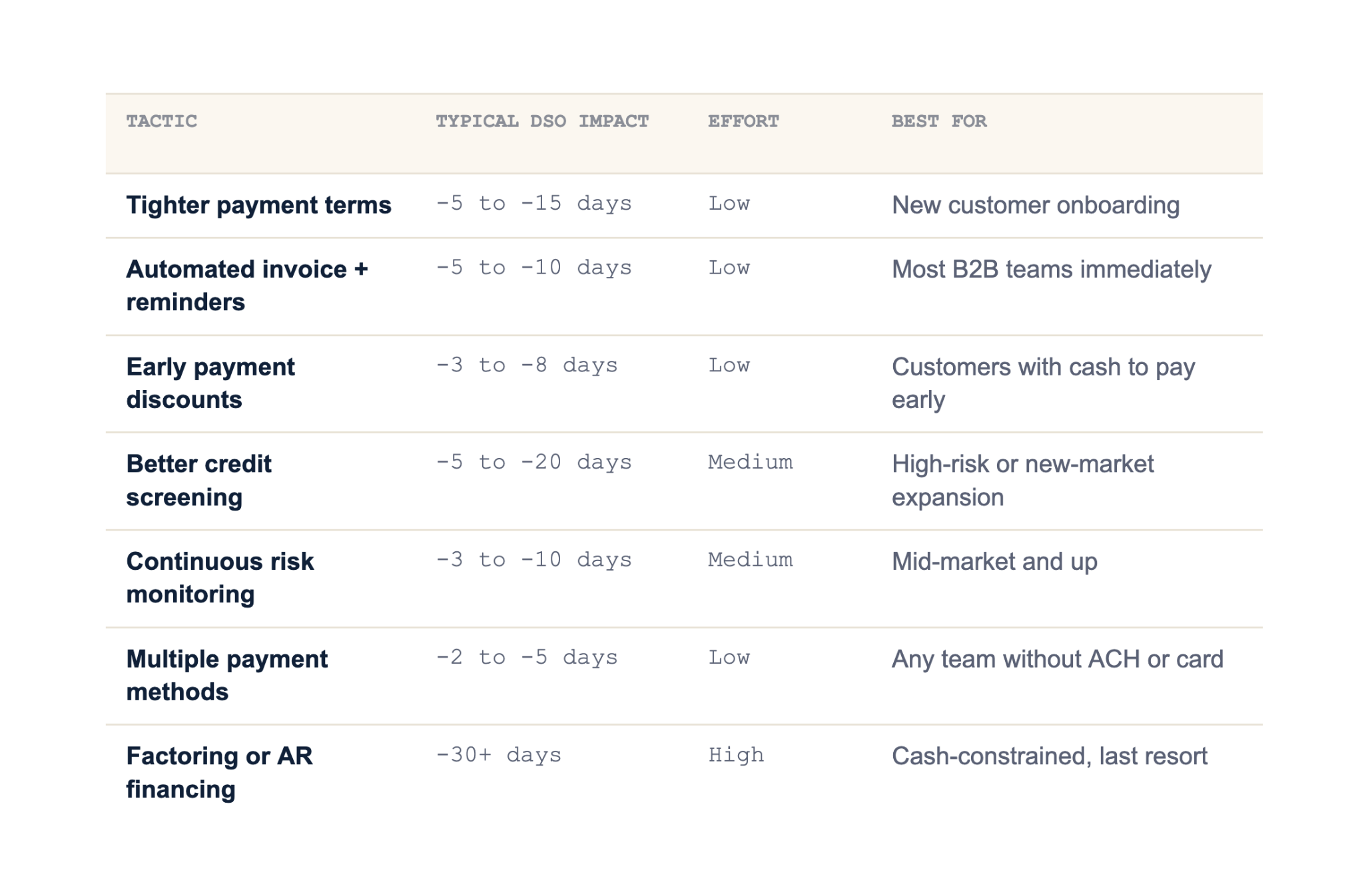

• The fastest wins come from automated reminders, multiple payment options, and tightening terms with new customers. Each can shave 5 to 10 days of DSO with low effort.

• Continuous credit monitoring catches deteriorating customers before they slip into late payment, which prevents DSO from getting worse in the first place.

• Track DSO alongside dispute rate, write-offs, and Best Possible DSO. Lowering DSO without watching those is how teams unintentionally damage customer relationships.

Direct Answer

The fastest way to lower Days Sales Outstanding is rarely the obvious one. Most teams default to chasing harder, which produces small gains and damages relationships. The bigger gains come from better decisions at the front of the cycle (who you extend credit to, what terms you offer) and consistent execution at the back (how invoices and reminders go out).

Across most B2B businesses, the highest-leverage tactics are: tightening payment terms with new customers, automating invoice delivery and reminders, adding multiple payment options, and layering continuous credit risk monitoring to catch deteriorating customers before they slip late. Each of these can shave 5 to 15 days off DSO with modest effort.

The honest constraint: lowering DSO past your industry's natural floor usually requires either tougher terms (which costs you customers) or external financing (which costs you margin). Track DSO alongside dispute rate and write-offs to make sure you're improving cash flow, not just shifting the problem.

Quick Comparison: DSO-Lowering Tactics

Key Definitions

• DSO (Days Sales Outstanding): The average number of days it takes to collect payment after a sale. Calculated as (Accounts Receivable / Total Credit Sales) x Number of Days.

• Best Possible DSO (BPDSO): The DSO you'd achieve if every customer paid exactly on terms with zero days late. The gap between actual DSO and BPDSO is your collections opportunity.

• Aging: Breaking down outstanding receivables by how overdue they are (current, 1-30, 31-60, 61-90, 90+). The shape of aging matters more than DSO alone.

• Dunning: The structured process of contacting customers about overdue invoices. Automated dunning sequences run reminders across email, SMS, and phone on a schedule.

• 2/10 net 30: A common early payment discount notation, meaning 2% off if paid within 10 days, otherwise net 30. The discount must be smaller than your cost of capital to make sense.

Step-by-Step: How to Run a DSO Reduction Project

1. Calculate your current DSO and BPDSO. Compare both to industry benchmarks. The gap between actual DSO and BPDSO tells you whether the problem is collections execution or terms structure.

2. Segment AR by customer. The Pareto rule almost always applies. Identify which 20% of customers cause 80% of DSO drag. Quick wins live there.

3. Audit invoice mechanics. How fast does an order become an invoice? How fast does an invoice reach the customer? Most teams have 2 to 5 days of avoidable delay before any reminders even start.

4. Automate the basics. Invoice delivery, payment reminders, late fee calculation, payment matching. Anything done manually is a candidate for automation.

5. Tighten new customer terms. Existing customer terms are hard to change. New customer terms are easy. Move new accounts to net-15 by default and only extend longer when there's a specific reason.

6. Add a credit monitoring layer. Catching deteriorating customers before they slip late prevents DSO from getting worse. This is where the credit risk side of the work matters most.

7. Review monthly, adjust quarterly. DSO is noisy month to month. Track the trend, not the spot. Compare against the same period last year, not just last month.

Common Mistakes

• Treating DSO as the only metric. A team that hits DSO targets by writing off receivables hasn't actually improved cash flow. Track DSO, dispute rate, and bad debt expense together.

• Pushing terms too aggressively. Net-15 across the board sounds clean. In practice, customers either negotiate back or leave. Targeted terms (by segment, risk tier, or relationship) work better.

• Automating dunning without segmenting. The same reminder cadence for a $500 invoice and a $50,000 invoice produces poor outcomes on both. Segment by amount, customer tier, and relationship age.

• Ignoring dispute resolution time. Disputed invoices are silent DSO killers. They sit unpaid, often unflagged, for weeks. Set an SLA on dispute resolution and track it monthly.

• Discounting more than you save. A 2% early payment discount equals roughly 36% annual interest. If your cost of capital is 12%, you're losing money. Run the math before standardizing discounts.

• Death by a thousand small accounts. Teams focus on the top 20 customers and ignore the long tail. Small balances accumulate. Automate the long tail aggressively.

Frequently Asked Questions

What's a good DSO for B2B businesses?

It depends on your industry and terms. As a rough guide: 30 days or below is excellent, 30 to 50 days is healthy for most B2B sectors, 50 to 70 days is common in manufacturing and distribution, and 70+ days suggests either structural issues or industries with naturally extended terms (construction, healthcare, government).

How quickly can I lower DSO?

Quick wins (automated reminders, multiple payment options, tighter new customer terms) can produce visible movement in 60 to 90 days. Structural changes (credit policy, AR platform, factoring) take 6 to 12 months to show full impact. Don't expect a one-month transformation. DSO improvement compounds over quarters.

Do early payment discounts actually work?

Sometimes. They work when the discount is smaller than your cost of capital and your customers have cash sitting in operating accounts. They don't work when customers ignore the discount and pay on terms anyway, which is common in industries where AP teams pay strictly by due date. Pilot before standardizing.

What's the difference between DSO and Best Possible DSO?

DSO measures actual collection speed. Best Possible DSO measures what your collection speed would be if every customer paid exactly on terms with zero late days. The gap between the two is your collections opportunity. If your DSO is 45 and your BPDSO is 35, you have 10 days of late payment to recover.

Should I use factoring or AR financing to lower DSO?

Factoring and invoice financing reduce reported DSO immediately by selling receivables to a third party. They don't actually fix the underlying cycle. Useful when cash flow is constrained and you need quick liquidity. Expensive over time. Treat as a working capital tool, not a DSO improvement strategy.

How does DSO relate to credit risk monitoring?

Continuous monitoring catches deteriorating customers before they slip late, which prevents DSO from rising in the first place. A customer whose LinkedIn headcount drops 15% and starts missing earnings guidance is the same customer who will be 30 days late on your next invoice. Acting on the early signal protects DSO.

What's the financial impact of lowering DSO by 10 days?

Roughly: 10 days of DSO equals about 2.7% of annual revenue tied up in working capital. For a $20M business, that's $548,000 of cash freed up. The exact number depends on your gross margin and collection seasonality, but the order of magnitude is consistent across most B2B businesses.

What to do next

1. Calculate your current DSO and BPDSO. The gap between them tells you where the work is.

2. Pick three Tier 1 quick wins from the framework above and run them this quarter. Don't wait for a platform decision.

3. If your DSO is rising because customers are deteriorating before they pay, see how Merclex layers credit risk monitoring on top of your existing AR workflow.