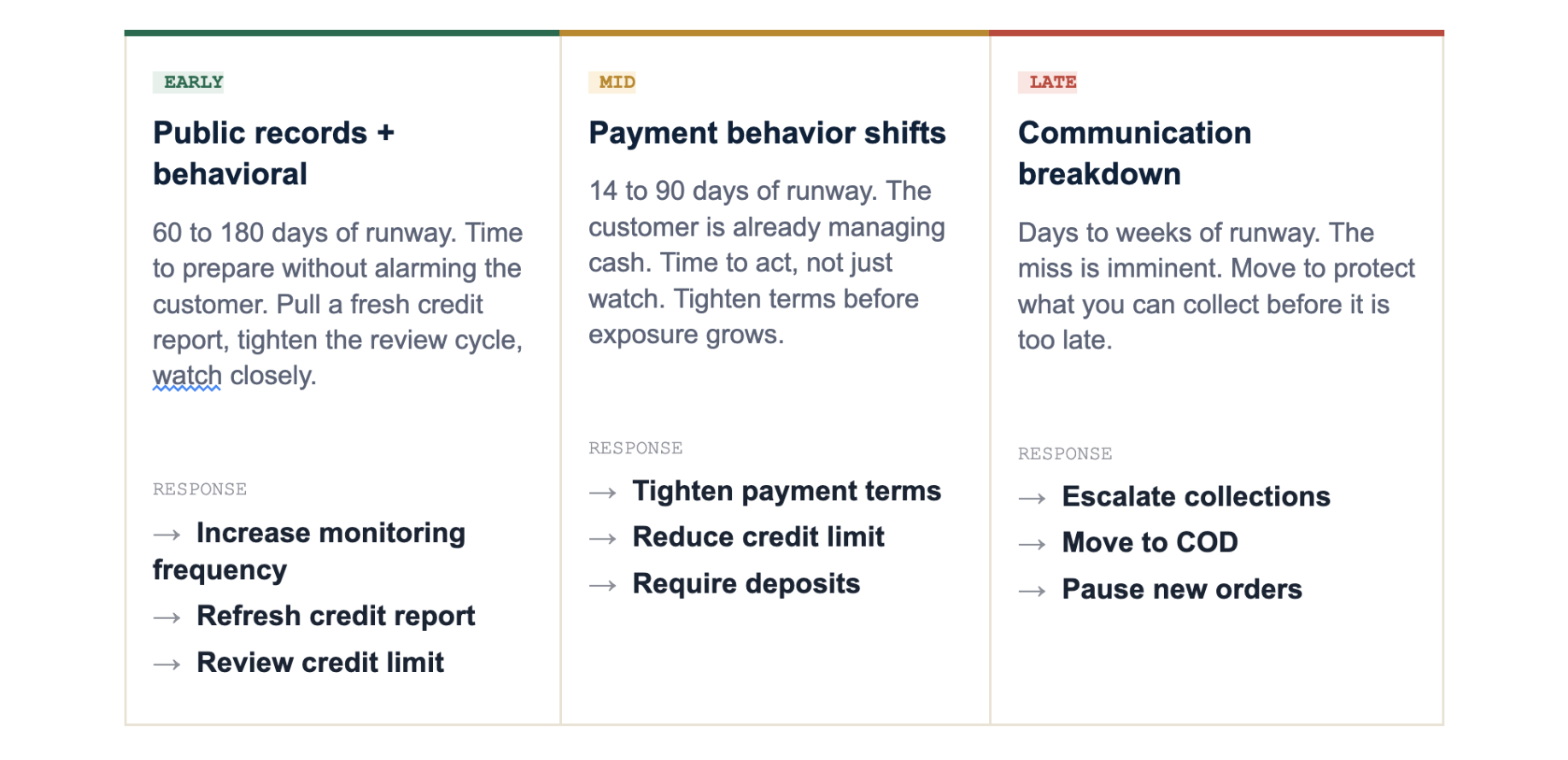

• Missed payments are usually preceded by signals across four categories: public records, behavioral signals, payment behavior, and communication patterns.

• Public records and behavioral signals (UCC filings, LinkedIn headcount drops, leadership departures) lead by 60 to 180 days. They are the earliest warnings.

• Payment behavior changes (DBT extending, partial payments) lead by 14 to 90 days. By then the trouble is already advanced.

• Communication shifts (slower responses, going dark) are the latest signals, often just days to weeks before a miss. By the time a customer stops replying, you are nearly out of runway.

Direct Answer

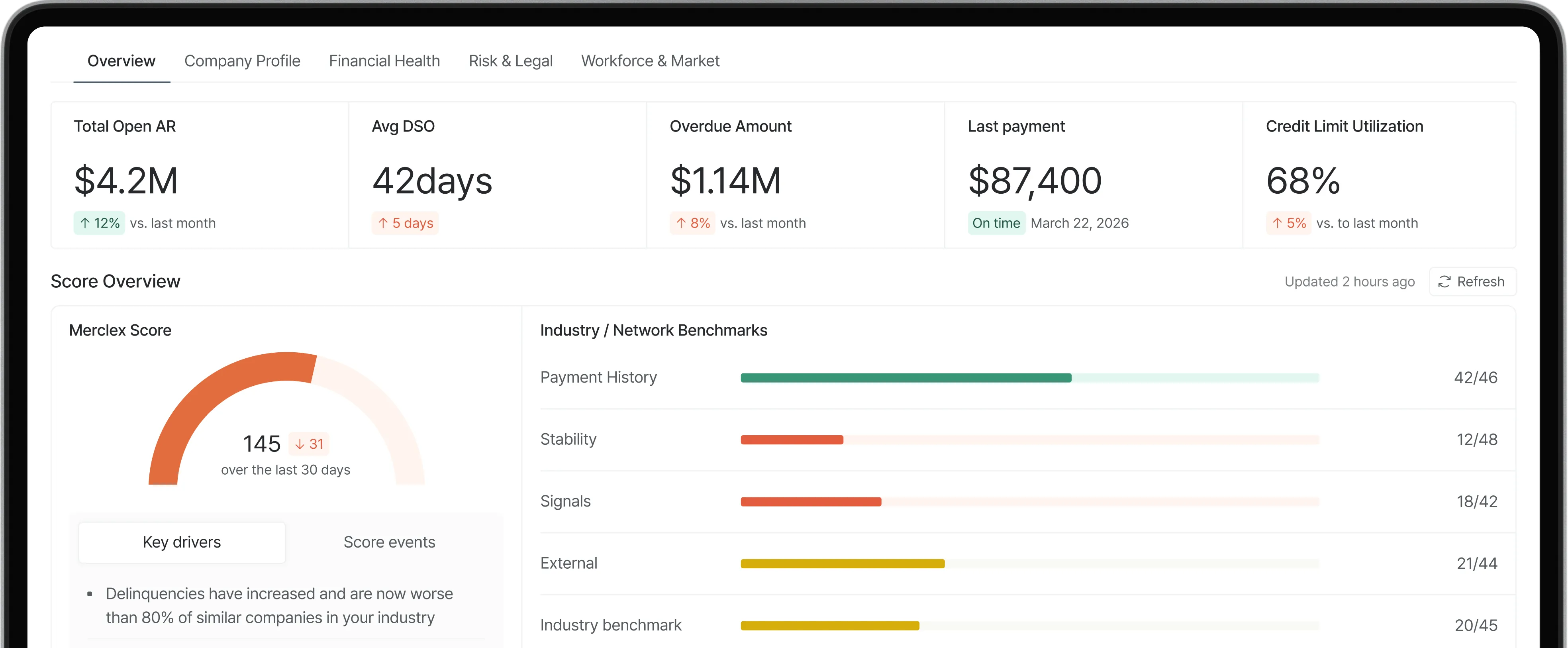

The earliest reliable signs that a business customer will miss payment come from outside your own AR data. Public records like new UCC filings, lawsuits, and tax liens, plus behavioral signals like LinkedIn headcount drops and leadership departures, typically appear 60 to 180 days before a missed payment. These are leading indicators because they reflect the underlying business deterioration before it reaches your invoice.

Your own data tells the story later. Payment behavior changes, days beyond terms (DBT) extending, partial payments appearing, dispute frequency rising, usually show up 14 to 90 days out. By the time you see these, the customer is already managing cash tightly. Communication signals, slower email responses and unreturned calls, are the last to appear, often within days or weeks of an actual miss.

The practical implication: if you only watch your AR aging report, you are watching a lagging indicator. The customers who blindside you are the ones whose external signals fired months ago while their payments stayed current right up until they did not.

The Four Signal Categories

1. Public Records (earliest, 60 to 180 days out)

• New UCC filings: A lender filing a UCC-1 against your customer means someone else extended secured credit. A sudden cluster of filings can indicate the business is raising cash against its assets.

• Lawsuits and judgments: Litigation, especially from other suppliers or lenders, signals the customer may already be failing to pay others. Judgments are an even stronger signal.

• Tax liens: Federal or state tax liens indicate the business is behind on tax obligations, usually a sign of serious cash flow stress. The IRS is rarely the first creditor to go unpaid.

2. Behavioral Signals (early, 45 to 180 days out)

• LinkedIn headcount drops: A sustained decline in employee count, especially above 10%, often precedes financial trouble. Layoffs are a cash conservation move.

• Leadership departures: A CFO or COO leaving without a named replacement is a notable signal. Finance leaders often leave before trouble becomes public.

• Negative news mentions: Coverage of restructuring, layoffs, lost contracts, or litigation. AI monitoring tools surface these faster than manual searching.

3. Payment Behavior (mid-stage, 14 to 90 days out)

• DBT extending: Days Beyond Terms creeping up by 5 or more days for two consecutive months is one of the most reliable predictors. It means the customer is stretching you specifically.

• Partial payments: A customer who used to pay in full starting to pay partially is managing cash. They are prioritizing which creditors to pay, and you are no longer at the top.

• Rising dispute frequency: A sudden increase in invoice disputes is often a stalling tactic. Disputes buy time without technically going past due.

4. Communication Patterns (latest, 3 to 60 days out)

• Slower email responses: A customer who used to reply within a day now taking a week. Avoidance is a behavioral tell that the conversation has become uncomfortable.

• Going dark on calls: Unreturned calls and unanswered emails about payment are among the last signals before a miss. By this point, intervention options are limited.

How to Act on the Signals

Match your response to how early the signal is. Early signals justify monitoring and preparation. Late signals justify immediate action.

Common Mistakes

• Watching only AR aging. By the time a customer is past due on your invoices, the leading signals have been firing for months. AR aging is a lagging indicator, not an early warning.

• Treating a single signal as decisive. One UCC filing might be routine financing. The pattern is what matters: multiple signals firing together across categories is the real warning.

• Ignoring communication tells. Finance teams often dismiss slower responses as the customer being busy. Combined with payment behavior changes, avoidance is a meaningful signal.

• Acting too late on early signals. The whole value of a 120-day-early signal is the runway it gives you. Teams that wait for confirmation lose that advantage and end up reacting at the same time as everyone else.

• Not having a defined response per signal. A signal without a predefined action is just anxiety. Decide in advance what each signal triggers, so the response is automatic rather than debated.

Frequently Asked Questions

What is the single most reliable early sign of a missed payment?

Days Beyond Terms (DBT) extending consistently is the most reliable signal that comes from your own data. When a customer's average days-to-pay creeps up by 5 or more days across two consecutive months, the probability of an eventual miss rises sharply. The catch is that DBT is a mid-stage signal. Public records and behavioral signals appear earlier but require external monitoring.

How far in advance can you predict a missed payment?

With external signal monitoring (public records, LinkedIn, news), 60 to 180 days is realistic for many customers. With AR data alone (payment behavior), 14 to 90 days. With communication signals only, days to weeks. The earlier you want to see it coming, the more you have to look beyond your own AR system.

Can these signals be monitored automatically?

Yes. Public records, LinkedIn changes, news sentiment, and payment behavior can all be monitored automatically by AI-driven credit platforms. The advantage of automation is catching the early signals (which require watching external sources continuously) rather than only the late ones (which show up in your own AR data anyway).

Is a customer asking to extend payment terms always a bad sign?

Not always. A term extension request can be routine cash flow management, especially for seasonal businesses. It becomes a warning when combined with other signals: a term request plus a LinkedIn headcount drop plus a slower payment trend is a different situation than a term request in isolation. Context matters.

What should I do when I see an early warning sign?

Match the response to the signal's lead time. Early signals (public records, behavioral) justify increased monitoring and a credit limit review, but not alarming the customer. Mid-stage signals (payment behavior) justify tightening terms or reducing exposure. Late signals (communication breakdown) justify moving to COD or escalating collections. The point is to act proportionally and early.

Do these signals work for small private customers?

Mostly yes, though the mix shifts. Public records and behavioral signals (LinkedIn, news) work for businesses of any size. Traditional credit scores are thinner for small private companies, which is exactly why behavioral and payment-behavior signals matter more for that segment. Watching your own AR data closely is especially important for small private customers.

Summary

• Missed payments are preceded by signals across four categories: public records, behavioral, payment behavior, and communication. Most fire well before the miss.

• Public records and behavioral signals lead by 60 to 180 days. Payment behavior leads by 14 to 90 days. Communication signals are last, often just days out.

• Watching only AR aging means watching a lagging indicator. The earliest warnings come from outside your own data.