• AI credit monitoring is better than traditional reports for catching deterioration early. Reports are still better for one-time decisions and structured documentation.

• AI brings three things reports can't: pattern recognition across many signals at once, NLP synthesis of news and earnings calls, and prioritization of which accounts actually need attention.

• Reports keep one durable advantage: they're the standard format auditors, credit committees, and lenders expect for decision documentation.

• Most B2B credit teams need both. Reports for the decision, AI monitoring for awareness between decisions.

Direct Answer

AI credit monitoring is better than traditional credit reports for one specific job: catching customer deterioration early enough to act on it. It's not better at everything, and it doesn't replace reports entirely. The two solve different problems.

Traditional credit reports excel at structured, point-in-time documentation. They're the format auditors expect, the format credit committees review, and the format you reference when justifying a credit decision in a dispute. The structure makes them defensible. The same structure makes them slow.

AI credit monitoring excels at the synthesis problem. A credit team monitoring 500 customers can't read every news article, every earnings call, every LinkedIn change. AI does that work continuously, pattern-matches across signals (payment behavior + headcount drop + negative news), and surfaces only the accounts that have materially shifted. That's a job reports were never designed to do.

The honest answer to which is better: AI monitoring is better at predicting trouble. Reports are better at documenting decisions. Most B2B credit teams need both.

Key Definitions

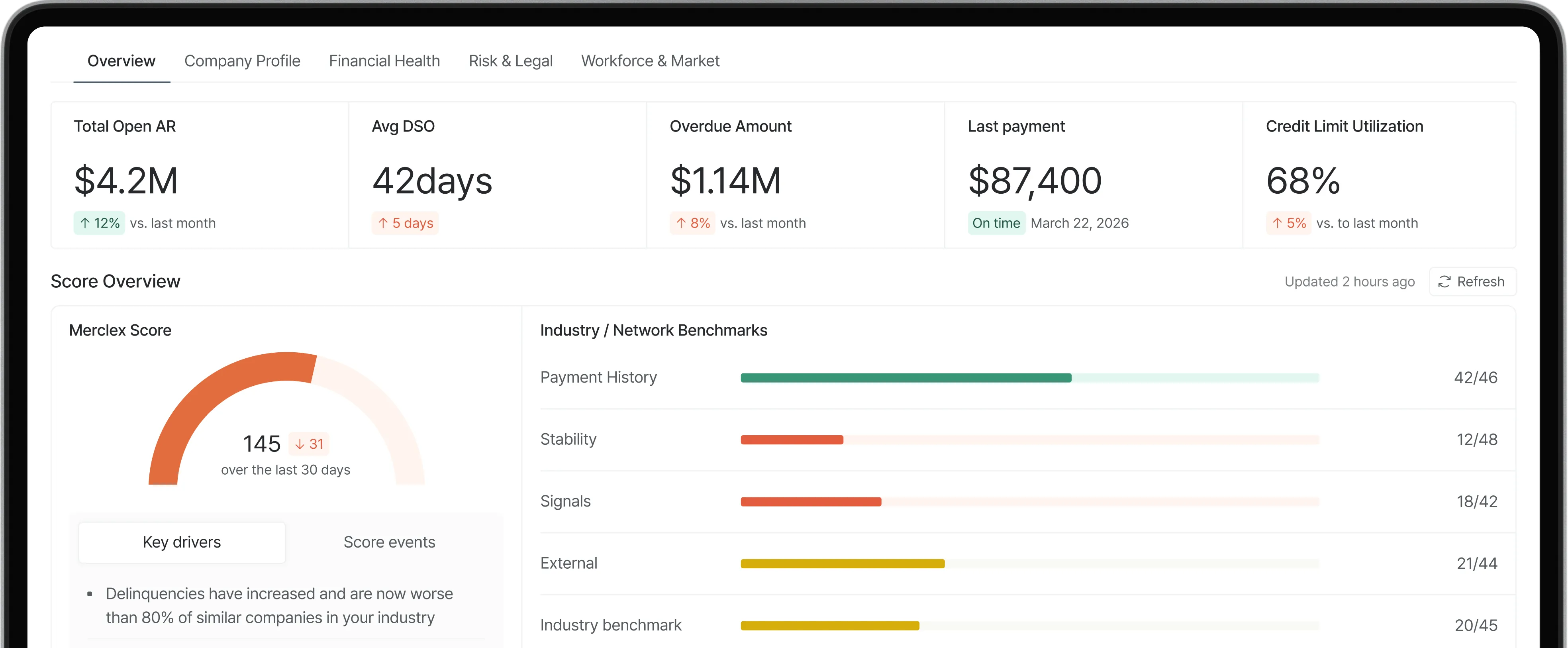

• AI credit monitoring: Continuous surveillance of customer risk using machine learning to synthesize across signals (payment behavior, news sentiment, LinkedIn data, earnings transcripts) and prioritize accounts.

• Traditional credit report: A structured document compiled by a bureau (D&B, Experian, Equifax, Creditsafe) summarizing a company's payment history, public records, financial profile, and credit score at a point in time.

• Pattern recognition: AI's core advantage. A 10% LinkedIn headcount drop alone is noise. A 10% drop combined with negative news and a one-week DBT increase is a signal. AI catches the combination.

• Natural language processing (NLP): What allows AI to read earnings call transcripts, news articles, and analyst reports and extract sentiment or risk language. Reports don't do this.

• Prioritization: The most useful AI feature for daily credit work. Instead of reviewing all 500 customers, AI surfaces the 5 that actually changed.

Step-by-Step: How to Use Both Together

1. Pull a credit report at onboarding. This is your decision document. It establishes the baseline for credit limit, terms, and any guarantees.

2. Enable AI monitoring on every approved customer. The cost per account is small. The upside is catching deterioration before it shows up in payment behavior.

3. Define what AI signals trigger a fresh report. A material AI alert (payment pattern shift + news event + headcount drop) should trigger a new report, not just a note.

4. Use reports for formal credit reviews. Annual on top exposures, semi-annual or quarterly on highest-risk customers. The structured format is what auditors and credit committees expect.

5. Feed AI alerts into AR workflows. When AI flags a customer, the AR team should know before the next collection call. Context changes how you collect.

6. Don't try to make AI monitoring replace reports for decision documentation. The structure of a credit report has legal and procedural value. AI is a complement, not a substitute.

Common Mistakes

• Treating AI monitoring as a replacement for reports. Reports still serve a documentation function AI hasn't replaced. Use both.

• Believing all "AI" is real AI. Many platforms market "AI credit monitoring" but run rule-based workflows underneath. Test whether the system actually adapts to new data, or just sends alerts when X happens.

• Buying AI without acting on alerts. AI monitoring only matters if alerts route to a human with authority to adjust terms, limits, or escalate. Otherwise it's expensive noise.

• Ignoring the audit trail. If you're in a regulated industry or sell to one, AI alerts alone won't satisfy auditors. Pair monitoring with periodic structured documentation.

• Comparing accuracy claims without context. "96% accuracy" on public company bankruptcy doesn't transfer to private company default. Match the claim to your portfolio.

Decision Framework: When Each Wins

AI monitoring and traditional reports each have situations where they're clearly the right tool. Most credit teams need both, but the weighting differs by use case.

Frequently Asked Questions

Is AI credit monitoring more accurate than traditional reports?

More accurate at predicting trouble in advance, yes. Reports measure what already exists in the data. AI monitoring catches signals that precede the data (headcount changes, news sentiment, payment pattern drift). For predicting which customer will fail in 6 to 12 months, AI monitoring outperforms reports. For confirming what's already true, reports are fine.

Can AI credit monitoring fully replace credit reports?

No, not yet. Reports are still the format auditors, lenders, and credit committees expect for documenting credit decisions. The legal and procedural role of a structured report hasn't been replaced. AI monitoring complements reports; it doesn't substitute for them in most workflows.

What signals does AI monitoring catch that reports miss?

Behavioral signals that aren't in credit data: LinkedIn headcount drops, leadership departures, news sentiment shifts, earnings call language changes, customer complaint patterns, social media signals. These appear 3 to 12 months before they show up in financials, which is when reports would catch them.

Is AI credit monitoring expensive compared to reports?

Depends on portfolio size. For small portfolios (under 50 customers), pulling reports as needed is cheaper. For larger portfolios, continuous AI monitoring is more cost-effective per account, because you're paying once for ongoing coverage rather than per-event for snapshots.

How do I know if AI monitoring is actually using AI?

Ask three questions. Does it synthesize across multiple signal types (not just credit data)? Does it prioritize accounts dynamically based on changing patterns? Does it adapt to customer-specific baselines? If the answer to all three is yes, it's doing real AI work. If it just sends alerts when a score changes, that's rule-based monitoring marketed as AI.

Do legacy bureaus offer AI monitoring or just reports?

Most of the major bureaus (D&B, Experian, Moody's) now offer monitoring add-ons that include some AI features. The quality varies. Newer specialized platforms (CreditRiskMonitor, Merclex) often have stronger AI monitoring capabilities because they were built for that use case rather than retrofitting AI onto a reports business.

Summary

• AI credit monitoring is better at predicting trouble. Traditional credit reports are better at documenting decisions. They solve different problems.

• AI brings three things reports can't: pattern recognition, NLP synthesis, and account prioritization. These catch deterioration 3 to 12 months earlier than reports.

• Most B2B credit teams need both. Reports for onboarding, credit committee reviews, and audit defense. AI monitoring for everything in between.

What to do next

1. Audit your current setup. Are you running both, or relying on reports alone?

2. If you only have reports, identify what would change in your credit decisions if you knew about LinkedIn headcount drops and news sentiment shifts as they happened.

3. If you're managing 50+ active customers and don't have AI monitoring, see how Merclex layers continuous AI monitoring on top of your existing bureau data.