- Running a business credit check on a new B2B customer means pulling a commercial credit report from a bureau (D&B, Experian Business, Equifax Business), reading the payment history and risk scores, and deciding whether to extend credit terms.

- You do not need consent to run a business credit check in the US, but you do need consent (under the FCRA) if you also pull the owner's personal credit.

- A single credit pull costs $39 to $200 depending on the bureau and report depth. A subscription runs $4,000 to $12,000 per year for a midsize business.

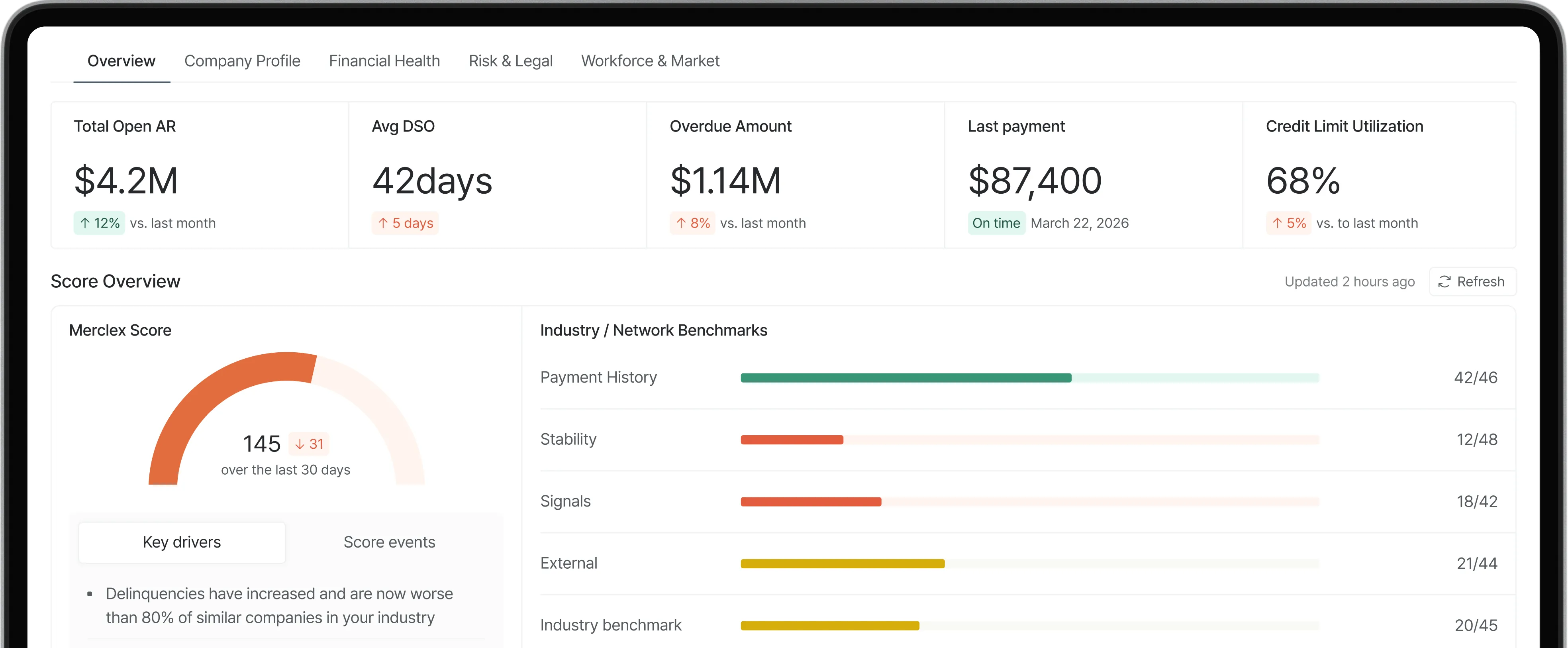

- The score is the start, not the finish. The fields that actually predict default are payment history, days beyond terms, recent legal filings, and contextual signals the bureaus do not track (LinkedIn headcount drops, leadership departures, news sentiment).

- A defensible business credit check process has six parts: a written credit policy, identifying information collection, the credit pull, contextual review, a documented decision, and ongoing monitoring.

How we put this guide together

This guide reflects months of evaluating the major credit bureaus against real B2B customer portfolios, mapping what each report actually catches versus what it misses, and pressure-testing the process AR and credit managers use day to day. The criteria below came from that work: speed, cost, decision usefulness, legal defensibility, and whether the data is fresh enough to matter.

What is a business credit check, and why does it matter for new B2B customers?

A business credit check is a process for pulling and reviewing a commercial credit report on a company you are about to do business with, usually to decide whether to extend trade credit, set payment terms, or accept the customer at all.

Unlike a personal credit check, a business credit check looks at trade payment behavior, public records (liens, judgments, bankruptcies), corporate structure, financial filings where available, and a proprietary risk score that predicts the probability of late payment or default. The major US business credit bureaus all publish their own scores: Dun & Bradstreet's PAYDEX (0 to 100), Experian's Intelliscore Plus (1 to 100), Equifax's Business Credit Risk Score (101 to 992), and Creditsafe's International Score (1 to 100).

The reason it matters for a B2B customer onboarding decision is simple math. According to the National Association of Credit Management (NACM), 43% of all US B2B credit sales are currently overdue, and 1% to 4% of accounts receivable are written off as bad debt every year. The US trade credit market is $5 trillion, larger than bank C&I loans and SME bank loans combined per Federal Reserve data. Most companies are extending more credit to other companies than banks are. Pretending you do not need to underwrite that exposure is how you end up writing off a six-figure invoice.

A business credit check is the cheapest insurance policy you have. A $50 to $200 report can prevent a five-figure or six-figure default.

When should you run a business credit check on a new B2B customer?

Run a business credit check before you extend any credit terms above your minimum threshold, before you onboard any customer expected to drive material revenue, and on a recurring basis for any active customer above a defined exposure level.

The four standard triggers:

- New customer onboarding. Anytime a customer asks for terms instead of cash on delivery or prepayment, run the check before approving.

- Credit limit increase requests. When an existing customer wants higher exposure (more inventory on terms, longer payment windows, or a larger PO), re-pull.

- Concentration thresholds. Anytime a single customer crosses a percentage of your AR (commonly 5% or 10%, depending on your risk tolerance), the relationship needs a fresh credit check and ongoing monitoring.

- Material change events. A customer's leadership change, a public layoff, a missed earnings call, or news of a lawsuit are all events that should trigger a re-check.

A defensible policy puts these triggers in writing and applies them consistently. Inconsistent application is the legal and operational risk you are trying to avoid.

How do you run a business credit check on a new B2B customer?

Running a business credit check on a new B2B customer is a seven-step process: write a credit policy, collect identifying information, choose a data source, pull the report, layer in contextual data, document the decision, and set up ongoing monitoring.

Step 1: Write a credit policy before you pull anything

Before you run a single report, your finance team needs a written credit policy that defines: what credit limits apply to which customer tiers, what triggers require a credit check, what documentation you collect from customers, what scores or signals trigger a decline, and what payment terms are available at each risk level.

For example: Tier A (score 80+) gets Net 60 up to $250K, Tier C (below 60) is prepay only. Without a written policy, every decision becomes ad hoc, exposing you to bias claims and inconsistent risk pricing.

A one-page policy is enough to start. The point is consistency, not length.

Step 2: Collect the customer's identifying information

You cannot pull a report without the right inputs. At minimum, you need:

- Legal entity name (not the DBA, the registered name)

- State of incorporation

- Federal Employer Identification Number (EIN), if available

- Headquarters address

- Years in business

- Owner or principal name (only required if you are also pulling personal credit, which requires consent)

Collect this with a credit application before extending terms. Merclex offers a free template built by thousands of credit pros in their community, so you are not designing one from scratch.

Step 3: Choose a credit data source

There are four credible sources for US business credit data: Dun & Bradstreet, Experian Business, Equifax Business, and Creditsafe. Each has different strengths and different pricing.

- D&B: deepest legal entity data, the D-U-N-S Number standard, weakest UX, highest price (single reports start around $189; subscriptions run six figures)

- Experian Business: best for sole proprietors and businesses with strong owner personal credit linkages; single Intelliscore reports run around $50 to $99

- Equifax Business: strongest when bundled with fraud and identity verification; less depth on pure trade payment data

- Creditsafe: the most user-friendly UX of the legacy bureaus; subscriptions run in the range of $6,000 - $25,000 a year for a midsize business.

Modern alternatives also exist. Tools like Merclex integrate directly with QuickBooks, Sage, and other ERPs to pull AR data automatically, then layer trade payment data on top of contextual signals (LinkedIn headcount, leadership changes, news sentiment) the legacy bureaus do not track.

For a one-time check on a single customer, an on-demand single report is the cheapest option. For more than three to five checks a month, a subscription pays for itself.

Step 4: Pull the credit report

This part is procedural. Log into the bureau, enter the customer's identifying information, confirm the entity match, select the report depth (basic, standard, or premium), and pay for the pull. Most reports return in under a minute.

The first thing to verify is the entity match. If the legal entity name, state of incorporation, and address do not all align with what the customer gave you, the report is on the wrong company. Reject the match and try again with cleaner data.

Step 5: Layer in the contextual data the report misses

The legacy bureaus track DBT, public records, and trade payment behavior. Those are necessary inputs. They are no longer sufficient.

The signals that actually predict default in 2026 are often outside the report:

- LinkedIn headcount trends. A 15% headcount decline in 60 days is a leading indicator the bureaus catch six months later, if at all.

- Leadership departures. A CFO leaving without replacement, or back-to-back exits in operations or finance.

- News sentiment. Lawsuits, regulatory actions, recalls, founder controversies.

- Web traffic decline. A 30% drop in organic traffic for a B2C-facing customer signals revenue compression.

- Customer concentration risk. If their top customer is your customer's customer, your exposure stacks.

Spending five minutes on LinkedIn, Google News, and SimilarWeb before approving a credit line on a six-figure customer is the most expensive five minutes you will not spend at the wrong moment.

Step 6: Make a documented credit decision

Decide whether to: extend full terms, extend partial terms (lower limit, shorter payment window), require a deposit or partial prepayment, require a personal guarantee, or decline credit entirely. Then document the decision in writing.

The documentation should include: the credit application, the credit reports pulled, the contextual data reviewed, the decision rule applied (which credit policy tier), the decision itself, and the date. This documentation is your defense against bias or discrimination claims if the customer disputes the decision later.

Step 7: Set up ongoing monitoring

A credit decision at onboarding is a snapshot. The customer's risk profile changes constantly. Without monitoring, you find out about a customer's financial trouble when they stop paying. By then it is too late.

The minimum is quarterly re-pulls on customers above a defined exposure threshold. The better practice is real-time alerting on payment behavior, public records, and contextual data. Most modern credit intelligence tools (including Merclex, CreditRiskMonitor, and the bureaus' premium tiers) offer this. Configure alerts for the events that actually matter to your business and route them to whoever owns the customer relationship.

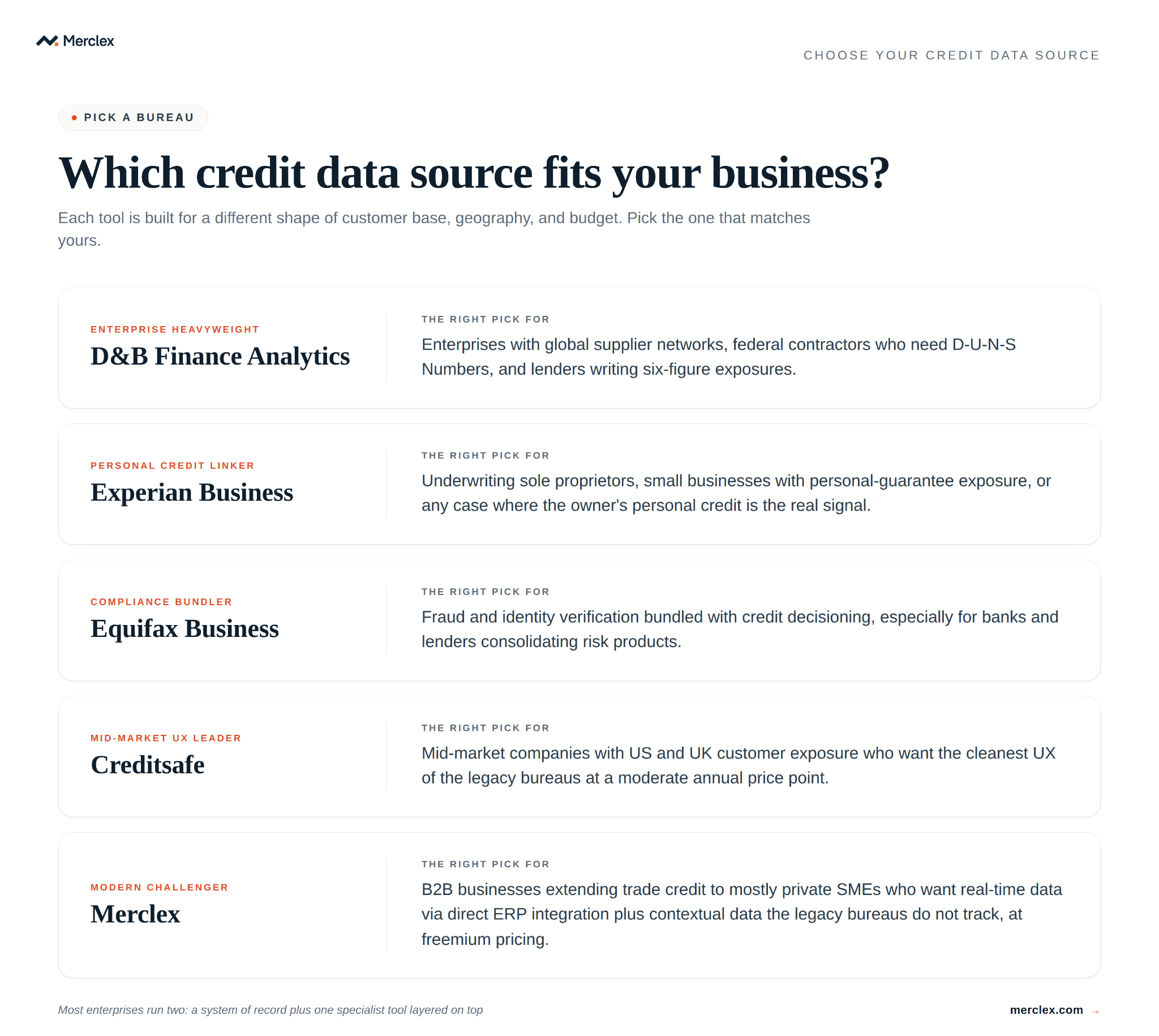

Which business credit bureau should you use?

The right business credit bureau depends on three things: the size of your customer (large enterprise, mid-market, or SME), your customer base's geography (US-only, US plus Europe, global), and your annual budget for credit data.

- D&B Finance Analytics is the right pick for enterprises with global supplier networks, federal contractors who need D-U-N-S Numbers, and lenders writing six-figure exposures.

- Experian Business is the right pick when you are underwriting sole proprietors, small businesses with personal-guarantee exposure, or any case where the owner's personal credit is the real signal.

- Equifax Business is the right pick when you need fraud and identity verification bundled with credit decisioning, especially for banks and lenders.

- Creditsafe is the right pick for mid-market companies with US and UK customer exposure who want the cleanest UX of the legacy bureaus at a moderate annual price point.

- Merclex is the right pick for B2B businesses looking for real-time signals and collections, as well as those extending trade credit to mostly private SMEs who want real-time data via direct ERP integration plus contextual data the legacy bureaus do not track, at freemium pricing.

Most enterprises end up running two systems: one of the bureaus as the system of record for legal entity data and trade payment behavior, plus one specialist tool layered on top for the gaps.

How do you read a business credit report?

A business credit report has four sections that actually drive the decision: identifying information, payment history, public records, and risk scores. The rest is supporting context.

Identifying information is the first section to verify, not the last. Confirm the legal entity name, the state of incorporation, the address, and the executive officers match what the customer provided. Mismatches mean either the customer is misrepresenting themselves, or the bureau matched the wrong company to your query.

Payment history is the section that actually predicts behavior. Look at the DBT (Days Beyond Terms), which is the average number of days the company pays its bills past the due date. A DBT of 0 means they pay on time. A DBT of 14 means they are a couple of weeks late on average. A DBT of 30+ means you should expect to chase invoices monthly.

Also look at the trend. A DBT moving from 5 to 25 over the last four quarters is worse than a steady DBT of 25. Trend matters more than the snapshot.

Public records are filings against the company: tax liens, mechanic's liens, civil judgments, UCC filings, and bankruptcy petitions. A single small lien is not a deal-breaker. Multiple recent liens, or any active bankruptcy filing, are.

Risk scores are the bureau's proprietary prediction of default probability. PAYDEX, Intelliscore Plus, Equifax Business Credit Risk Score, and Creditsafe's International Score all answer the same fundamental question with slightly different methodologies: how likely is this company to fail to pay you. Use the score as a screen, not as the final answer.

What red flags should make you restructure or decline credit?

Restructure terms or decline credit if you see any of these in the report or surrounding context: a steeply rising DBT trend, multiple recent liens or judgments, an active bankruptcy filing, ownership or leadership changes in the last 90 days, a steep LinkedIn headcount decline, or a credit score below the bureau's "high risk" threshold.

The five red flags that matter most:

- Rising DBT trend over the last four quarters. A company sliding from 5 days late to 30 days late is paying its other vendors first and you second.

- Multiple recent legal filings. One small lien is normal. Three filings in 12 months means lawyers are circling.

- Active bankruptcy or recent emergence. Companies just out of Chapter 11 are statistically much more likely to re-file within 24 months.

- Material concentration with a deteriorating customer. If their largest customer is in trouble, they are next.

- Ownership or leadership turnover without explanation. Especially CFO departures.

Any one of these is a reason to ask harder questions. Two or more is a reason to require a deposit, a personal guarantee, or to walk.

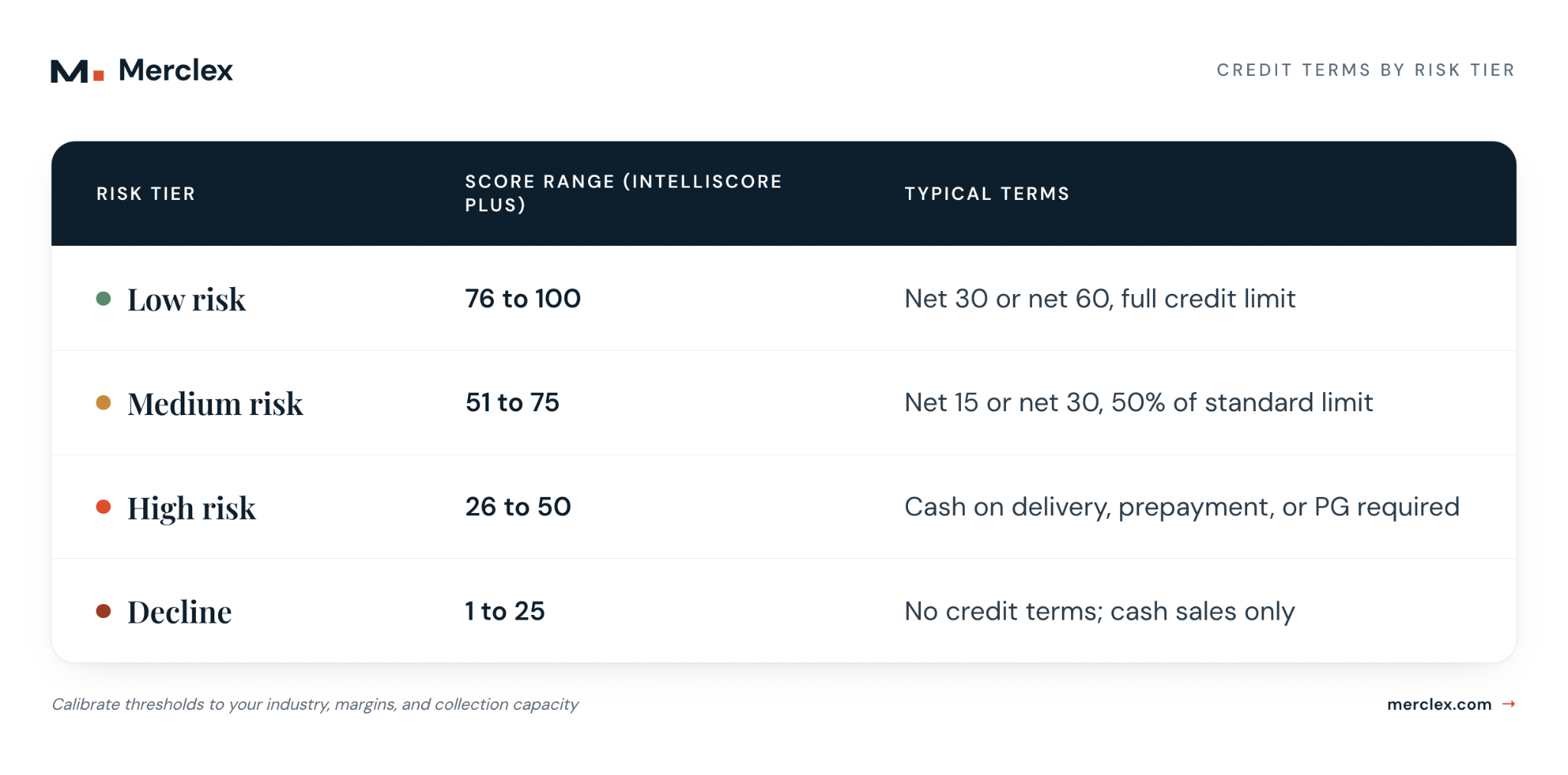

What credit terms should you offer based on the credit check?

Match credit terms to the risk tier the report indicates: low risk gets standard terms, medium risk gets reduced limits or shorter windows, high risk gets cash on delivery or prepayment, and decline categories get no terms at all.

A typical four-tier framework:

This is a starting point, not gospel. Calibrate the thresholds to your industry, your margins, and your collection capacity. A high-margin software company can absorb more risk than a low-margin distributor.

The other lever is the credit limit itself. Most companies set the initial limit at 10% to 20% of the customer's expected annual purchase volume, then increase it after a clean payment track record (typically 6 to 12 months).

Do you need consent to run a business credit check?

You don’t need the customer's consent to run a business credit check on their company in the United States, because business credit data is treated as public information. You do need explicit written consent if you also want to run a personal credit check on the owner or any guarantor, because personal credit data is protected by the Fair Credit Reporting Act (FCRA).

Most companies fold the personal credit consent language directly into the credit application. The customer signs the application, which includes a clause authorizing personal credit pulls on the named principals. This is the cleanest pattern and gives you the option to layer personal credit underneath the business credit when the situation calls for it (sole proprietors, small LLCs, personal-guarantee structures).

If you skip the consent and pull personal credit anyway, you are violating the FCRA. Penalties can include statutory damages, actual damages, and attorney's fees. Get the signed consent on file before you pull.

This guide is informational and not legal advice. If your customer base spans multiple jurisdictions or you are extending credit in regulated industries, talk to your counsel about specific consent and disclosure requirements.

How has the business credit check process changed in 2026?

The business credit check process in 2026 looks different from the one your AR team learned in 2015 in three meaningful ways: the underlying data is more contextual, the pull mechanism is more automated, and the monitoring is more real-time.

Three structural shifts:

- Data has moved from monthly to real-time. The legacy bureaus rely on AR managers manually exporting and emailing monthly invoice files to the network. Industry interviews suggest only 10 to 20% of customers actually do this, which means the trade data you are pulling is often stale by 30 to 60 days. Modern tools integrate directly with QuickBooks, Sage, and NetSuite to pull AR data automatically, which closes the participation gap and refreshes the network in real time.

- Contextual signals are now table stakes. LinkedIn headcount trends, leadership changes, news sentiment, web traffic, and Google review patterns are the leading indicators of distress. The bureaus track lagging indicators (filings, judgments, payment history). Both matter; only one of them was available to a 2015 AR team.

- Monitoring is automated. A 2015 process re-pulled credit reports quarterly. A 2026 process gets alerted in real time when something material happens to a customer, with AI prioritizing what actually matters versus what is noise.

The mechanics of running a business credit check have not changed: you still gather identifying information, pull a report, read the payment history, and make a decision. What has changed is the speed, the data depth, and the cost of doing it well.

Frequently asked questions about how to run a business credit check

How do you run a business credit check for free?

You can run a basic business credit check for free using government registries and public sources: SEC EDGAR for public company filings, state secretary of state filings for incorporation status and business standing, court records for active litigation and judgments, and free business lookup tools for identifying information. You will not get a proprietary risk score this way, but you will catch most of the legal red flags. Modern freemium tools also offer free tiers in exchange for contributing your own AR data to the network.

How long does it take to run a business credit check?

A standard business credit check takes between 30 seconds and 5 minutes once you have the customer's identifying information. The bureaus return reports instantly. The longer part of the process is collecting accurate identifying information from the customer (especially the EIN) and reviewing the report against your credit policy.

What is a good business credit score?

The threshold for "good" depends on the bureau. On Dun & Bradstreet's PAYDEX (0 to 100), 80 and above is considered low risk. On Experian's Intelliscore Plus (1 to 100), 76 and above is low risk. On Equifax's Business Credit Risk Score (101 to 992), 892 and above is low risk. As a general rule, a score in the top 25% of the bureau's range indicates a customer who pays on time consistently.

Can I run a business credit check on a sole proprietor?

A sole proprietor often has a thin or non-existent business credit file because the business and the owner are legally the same entity. In these cases, the more useful pull is the owner's personal credit report, which requires written consent under the FCRA. Experian Business specifically links consumer and business credit data, which is why it tends to be the right bureau for sole-prop underwriting.

How much does it cost to run a business credit check?

A single one-time business credit report costs between $39 and $200 depending on the bureau and the report depth. D&B's premium reports run higher (around $189 for a single comprehensive pull). Equifax single reports start around $99. Subscriptions run $4,000 to $12,000 per year for a midsize business with monthly pull volume. Enterprise contracts at D&B start in the low six figures. Freemium options exist for businesses willing to contribute their AR data to a network.

Do business credit checks affect the company being checked?

No. Unlike personal credit, business credit reports do not have a "hard inquiry" mechanism that lowers the subject's score when someone pulls them. A business can be checked unlimited times without any impact on its credit profile.

How often should I re-check existing customers?

Re-check customers above your concentration threshold quarterly at minimum. For top-tier customers (5%+ of AR or 10%+ of revenue), set up real-time monitoring instead of relying on quarterly pulls. Material change events (leadership exits, public layoffs, lawsuits) should trigger an immediate re-check regardless of the schedule. Merclex tracks these signals in real time and surfaces a credit review reminder the moment something changes.

What is the difference between a business credit check and a business credit monitoring service?

A business credit check is a one-time pull on a single company at a single point in time. A business credit monitoring service watches one or more companies continuously and alerts you when something material changes (a new lien, a missed payment to another vendor, a leadership change, a news event). Most companies use checks at onboarding and monitoring throughout the relationship.

Can a customer dispute the result of a business credit check?

A customer can dispute the underlying data on their own credit report directly with the bureau. They cannot dispute your decision to extend or deny credit based on that report, as long as you applied your written credit policy consistently and documented the decision. This is why a written credit policy and consistent application matter for legal defensibility.

What does DBT mean on a business credit report?

DBT (Days Beyond Terms) is the average number of days the company pays its invoices past the due date. A DBT of 0 means they pay on time, a DBT of 30 means they are typically a month late. DBT is the single best leading indicator of default risk and the most important number on the report.

Should small businesses run business credit checks?

Yes. Small businesses are often the most exposed to bad debt because a single defaulted customer can represent 5% to 20% of receivables. The cost of a single credit pull ($39 to $99) is trivial relative to the cost of writing off a five-figure invoice. Modern freemium options also make ongoing monitoring affordable for small businesses for the first time.

Merclex is a credit intelligence platform for B2B finance teams. It pairs traditional trade payment data with contextual signals and integrates directly with QuickBooks, Sage, and other ERPs to deliver real-time monitoring at freemium pricing.