HOW IT WORKS

• AI credit monitoring pulls signals from five categories continuously: traditional credit data, payment behavior, LinkedIn and workforce signals, news and sentiment, and earnings filings.

• An AI synthesis layer applies pattern recognition, NLP, and cross-signal scoring to turn raw data into prioritized alerts. Not every signal becomes an alert, and not every alert is equal.

• The output is a ranked list of accounts that actually need attention, not 200 alerts a day. The job is to surface the 5 that matter.

• What separates real AI monitoring from rule-based alerts is the synthesis across signal types. "Score dropped 10 points" is a rule. "Score dropped and headcount fell and news sentiment shifted" is a pattern only AI catches reliably.

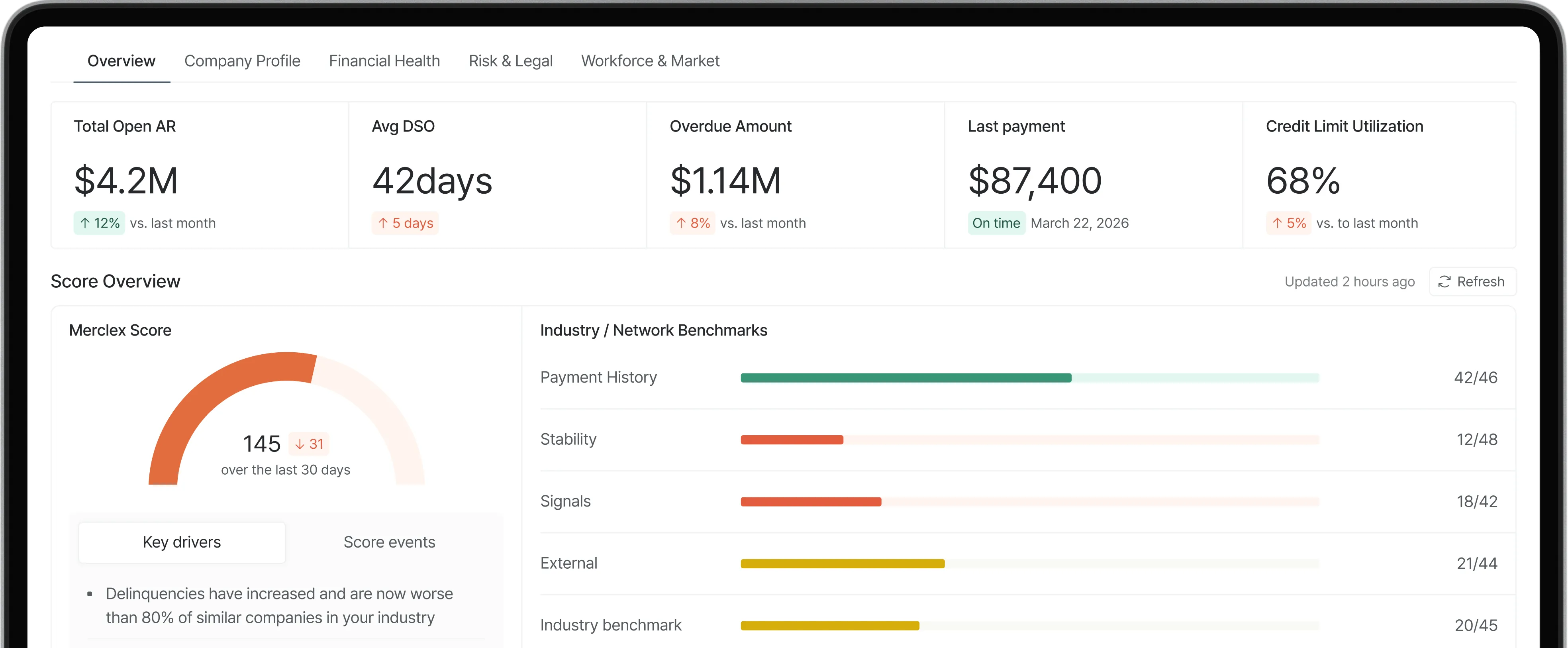

How Does AI Credit Monitoring Work for Finance Teams?

HOW IT WORKS

• AI credit monitoring pulls signals from five categories continuously: traditional credit data, payment behavior, LinkedIn and workforce signals, news and sentiment, and earnings filings.

• An AI synthesis layer applies pattern recognition, NLP, and cross-signal scoring to turn raw data into prioritized alerts. Not every signal becomes an alert, and not every alert is equal.

• The output is a ranked list of accounts that actually need attention, not 200 alerts a day. The job is to surface the 5 that matter.

• What separates real AI monitoring from rule-based alerts is the synthesis across signal types. "Score dropped 10 points" is a rule. "Score dropped and headcount fell and news sentiment shifted" is a pattern only AI catches reliably.

Direct Answer

AI credit monitoring works by continuously ingesting data from many sources, applying machine learning and natural language processing to look for patterns that precede default, and surfacing prioritized alerts to a human credit analyst. The core insight that makes AI useful here is that no single signal predicts trouble reliably, but combinations of signals do. A traditional credit score change might be noise. A score change combined with a LinkedIn headcount drop and negative news in the same week is usually not.

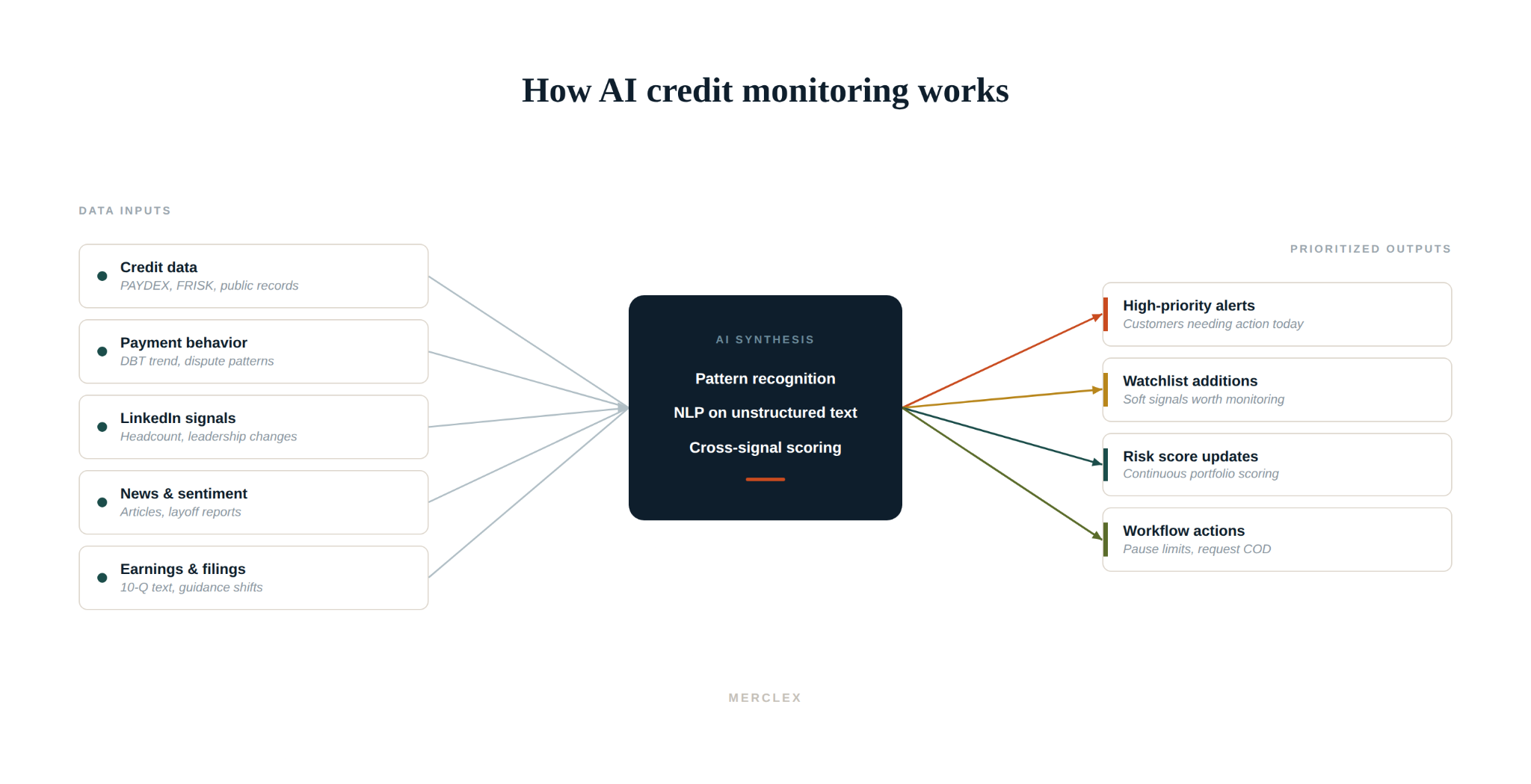

In practice, the workflow has three parts: inputs, synthesis, and outputs. Inputs include traditional credit data (PAYDEX, FRISK, public records), payment behavior data from the finance team's own AR system, LinkedIn signals like headcount and leadership changes, news and sentiment from public sources, and earnings filings text for public customers. The synthesis layer is where the AI lives; pattern recognition, NLP on unstructured text, and cross-signal scoring all happen here. The outputs are prioritized alerts ranked by urgency and confidence.

The expected payoff is documented. Financial Models Lab reported an 18% average reduction in bad debt write-offs in FY 2025 for firms using predictive credit scoring that includes behavioral signals. Resolve's analysis documents a 30% reduction when AR automation is combined with predictive monitoring. AI is a force multiplier, not a substitute for credit judgment.

The AI Monitoring Workflow

Three layers: data inputs, the AI synthesis brain, and prioritized outputs that flow into a human credit workflow.

How AI synthesizes five signal types into prioritized outputs for finance teams.

The Five Data Inputs

Each signal type tells the AI something different. None alone predicts default. The combination is what AI is built to read.

STAGE 01

Traditional credit data

Payment scores like D&B's PAYDEX, Experian's Intelliscore, and CreditRiskMonitor's FRISK Score. Public records: UCC filings, lawsuits, judgments, bankruptcies. This is the foundation, but it is largely lagging. By the time a credit score moves materially, the underlying business has often been deteriorating for months.

STAGE 02

Customer payment behavior

Days Beyond Terms (DBT) trend on your AR, dispute patterns, partial payments, payment timing relative to invoice age. This data lives in your own AR system. It is the most actionable signal because it is specific to your customer-vendor relationship, not a generic market signal.

STAGE 03

Workforce and leadership signals

LinkedIn headcount tracked over time. Leadership departures, especially CFO and COO exits without named replacements. Hiring slowdowns. Public posts about layoffs or restructuring. Workforce changes often precede financial trouble by months, which is why behavioral platforms invest heavily in this signal type.

STAGE 04

News and sentiment analysis

AI reads news articles, press releases, and industry coverage looking for language patterns associated with risk. Mentions of layoffs, restructuring, lawsuits, dispute coverage, supplier issues. NLP extracts sentiment from unstructured text, which is something rule-based monitoring cannot do reliably.

STAGE 05

Earnings calls and SEC filings (for public companies)

10-Q and 10-K filings, earnings call transcripts, and analyst Q&A. AI parses the text for guidance withdrawals, going concern language, debt covenant disclosures, and shifts in management tone. This signal type only works for public companies and their reporting subsidiaries.

AI Synthesis: What the System Actually Does

The synthesis layer is where AI credit monitoring earns its name. Three distinct functions happen here, all simultaneously and continuously.

• Pattern recognition: Machine learning models look for combinations of signals that historically preceded customer defaults. A single signal is noise. A pattern of signals firing together is signal. The model learns these patterns from training data, not from hard-coded rules.

• Natural language processing (NLP): Unstructured text from news, earnings, and filings is parsed for risk-relevant language and sentiment. NLP extracts meaning that simple keyword matching cannot. It can tell the difference between "the company is restructuring its debt" and "the company is restructuring its product portfolio."

• Cross-signal scoring: Every customer gets a continuously updated risk score that incorporates all signal types. The score is dynamic, not periodic. It moves when any underlying input moves. The system also calibrates confidence levels, distinguishing high-certainty alerts from soft signals worth watching.

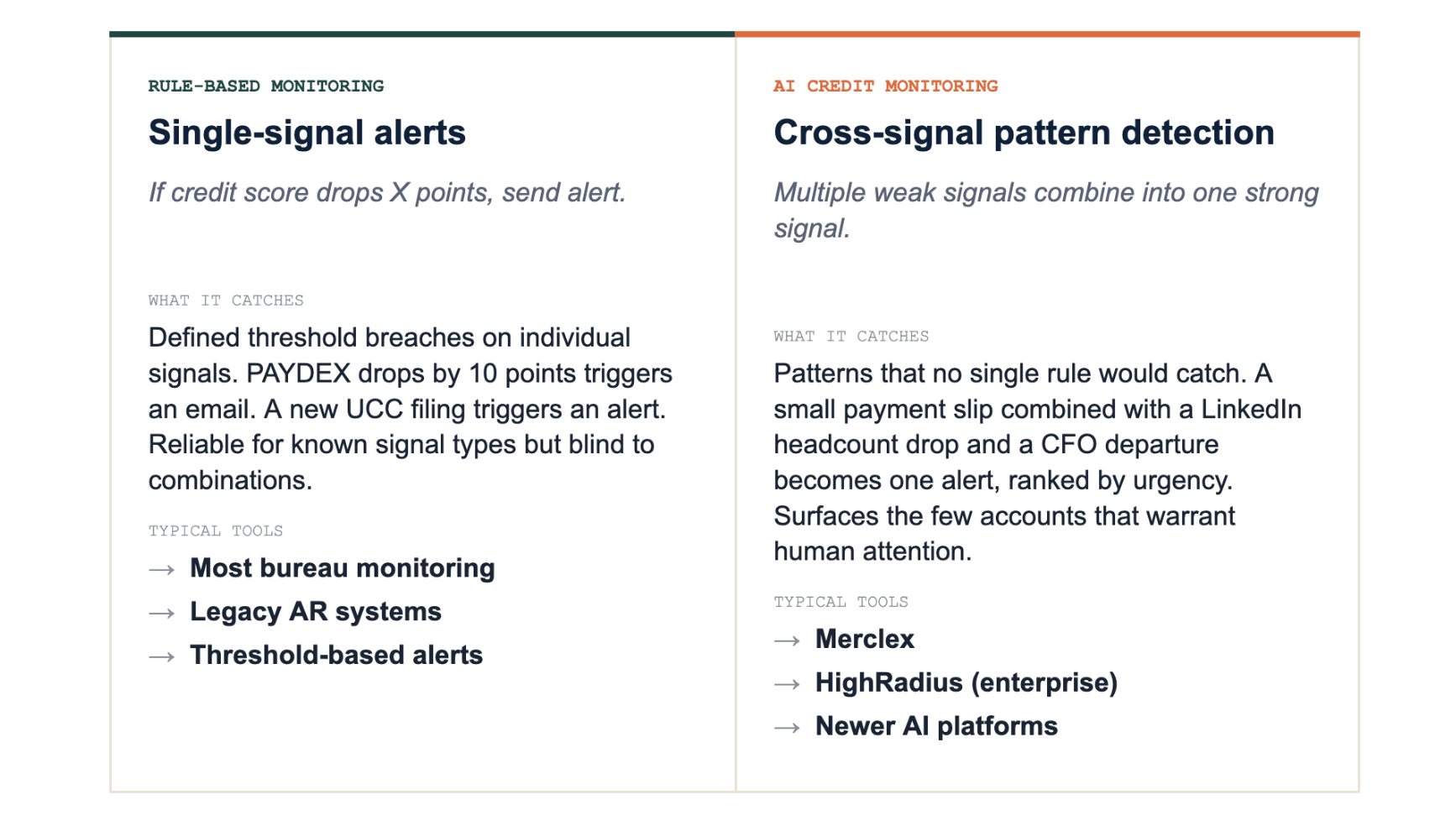

What Makes It Different From Rule-Based Monitoring

Most legacy bureaus offer monitoring features. Some are AI-driven. Most are rule-based. The difference matters more than the marketing suggests.

Common Mistakes

• Assuming "AI monitoring" always means real AI. Many platforms market AI features that turn out to be rule-based alerts dressed up in modern UI. Ask vendors specifically: does it adapt to new patterns over time, or does it fire when X happens?

• Treating AI alerts as decisions. AI surfaces accounts that need human attention. The credit decision still belongs to a human analyst with context about the relationship, the order size, and the strategic value of the customer.

• Tolerating false positives indefinitely. Early deployment of any AI system produces noise. The right response is threshold tuning and feedback, not learned helplessness. If 60% of alerts are noise after 90 days of tuning, something is wrong with the configuration or the underlying signal.

• Ignoring the human review step. AI without human review tends to overreact to short-term signals. A LinkedIn headcount drop in December might be year-end seasonality, not distress. Human judgment fills in context.

• Buying AI monitoring and not changing the workflow. The alert is the start of an action, not the end. Teams that buy AI monitoring and continue running monthly batch credit reviews capture maybe 20% of the value. The other 80% comes from triggered intervention.

Frequently Asked Questions

What is the difference between AI credit monitoring and traditional credit monitoring?

Traditional monitoring fires alerts when a specific signal crosses a defined threshold ("score dropped 10 points"). AI monitoring combines many signals using machine learning and surfaces patterns no single rule would catch. The practical difference: AI catches deterioration earlier because it sees combinations of weak signals before any single signal triggers a rule.

How accurate is AI credit monitoring?

Accuracy varies by platform and customer type. CreditRiskMonitor reports the FRISK Score at 96% accurate on public company bankruptcy three months out. Financial Models Lab documents an 18% reduction in write-offs from predictive credit scoring. Private company accuracy is lower because the underlying behavioral data is thinner; expect 70 to 85 percent accuracy at six to twelve month horizons.

What data does AI credit monitoring actually use?

Five categories: traditional credit data (scores, public records), payment behavior (DBT, disputes), LinkedIn signals (headcount, leadership), news and sentiment, and earnings filings for public companies. Different platforms emphasize different inputs. Bureau-based platforms lean on credit data and payment behavior. Newer AI-native platforms lean more on LinkedIn, news, and NLP.

Can AI predict bankruptcy?

Public company bankruptcy is the easiest case because the underlying data is rich and the patterns are well-studied. Reported accuracy for the leading scores is 90+ percent at three months out. Private company bankruptcy prediction is harder, with most platforms reporting 70 to 85 percent accuracy at six to twelve month horizons. "Predict" is the right word at the portfolio level; on any single customer, the result is a probability, not a certainty.

How do I know if a platform is using real AI versus marketing claims?

Three diagnostic questions. First, does the system synthesize across multiple signal types (not just credit data)? Second, does it adapt to changing patterns over time, or just fire alerts on fixed thresholds? Third, does it perform NLP on unstructured text? If the answer to all three is yes, it is probably doing real AI work. If it just emails when a score changes, that is rule-based monitoring marketed as AI.

Will AI replace credit analysts?

Not in any documented case study. The credit analyst's job changes: less manual file review, more triage of AI-surfaced alerts. Resolve's AR automation analysis and case studies from Bectran and HighRadius all describe the same pattern: analysts spend less time on data gathering and more time on judgment-heavy work like negotiating terms, structuring deals, and managing customer relationships.

How fast can AI monitoring detect trouble compared to traditional monitoring?

AI monitoring picks up behavioral signals 3 to 12 months before they show up in traditional credit scores. LinkedIn headcount drops, leadership changes, and news sentiment shifts are leading indicators. Credit scores and public records are lagging indicators. The earlier detection window is the main reason AI monitoring has measurable write-off reduction in published research.

Does AI credit monitoring work for private companies?

Yes, often better than traditional monitoring does for private companies. Bureau credit data on private companies is typically thin, especially for smaller businesses. Behavioral signals (LinkedIn, news, sentiment, payment behavior on your own AR) work regardless of whether the customer is public or private. This is why AI-native platforms tend to outperform bureau-only platforms on private B2B portfolios.