QUICK TAKE

• Bad debt prevention is a funnel: credit screening, limit setting, continuous monitoring, early intervention, then collections. Write-off is the last 5 to 10% that gets through.

• Most finance teams treat collections as the prevention strategy. By the time collections happens, prevention has already failed.

• The highest-leverage interventions are at the top of the funnel: credit screening at onboarding and continuous monitoring on existing customers. Each can prevent more bad debt than collections automation.

• Strong controls keep B2B write-offs below 0.5% of revenue. Weak controls let them climb above 1.8%. The gap is mostly about prevention discipline, not collections firepower.

Direct Answer

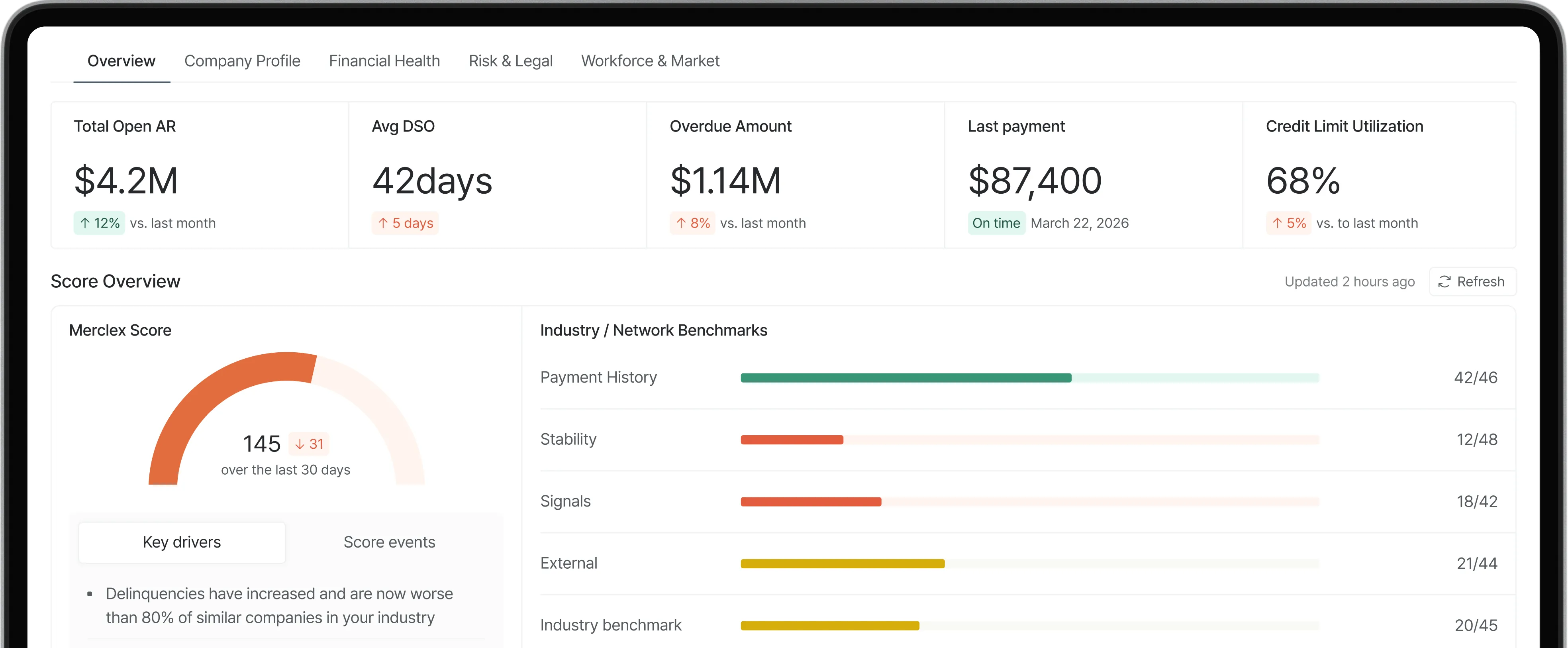

Finance teams prevent bad debt write-offs by treating prevention as a multi-stage funnel rather than a single workflow. The stages are: rigorous credit screening at onboarding, conservative credit limit setting, continuous monitoring of customer health, early intervention when signals shift, and disciplined collections. By the time an account reaches active collections, the prevention work has either succeeded or failed.

The pattern repeats across published research. Atradius's 2025 Payment Practices Barometer puts global B2B write-offs at around 6% of invoices. Financial Models Lab research shows that strong credit controls keep write-offs below 0.5% of revenue, while weak controls let them climb past 1.8%. The 3x gap between the two has very little to do with collections firepower and almost everything to do with what happens before terms are extended.

The honest version: prevention is unglamorous. Tightening onboarding, monitoring quietly, intervening early. Teams that invest in these stages have fewer dramatic collection battles because they didn't onboard the customers who would have created them.

Step-by-Step: The Prevention Workflow

1. Build a structured credit application. Every new customer fills it out. Include trade references, financials (where appropriate), and a clear statement of terms. This is the single most important prevention document.

2. Run rigorous screening before extending terms. Pull a credit report, check for UCC filings and recent lawsuits, verify trade references. The work here prevents more bad debt than any downstream automation.

3. Set conservative initial credit limits. New customers earn higher limits over time through demonstrated payment behavior, not at onboarding. Most write-offs trace back to over-extended initial limits.

4. Enable continuous monitoring on every active customer. The cost per account is small. The upside is catching deterioration before it shows up in payment behavior or, worse, in collections.

5. Define what triggers intervention. A monitoring alert isn't an action unless you've defined what action it triggers. Common triggers: DBT increase >5 days, leadership departure, headcount drop >10%, news of layoffs or litigation.

6. Intervene early when triggers fire. Options include tightening terms (net-30 to net-15), shortening review cycles, requiring deposits, or pausing further credit. Better to act early than wait for confirmation.

7. Treat write-off as feedback. Every write-off contains lessons about the prevention funnel. Was the screening too lax? Did monitoring miss the signal? Was intervention too slow? Document and adjust.

Common Mistakes

• Treating collections as the prevention strategy. Collections recovers some losses, but the math heavily favors prevention. A dollar spent on screening prevents more bad debt than a dollar spent on chasing.

• Over-extending initial credit limits. A new customer asking for high limits should be a yellow flag, not a green light. Conservative initial limits, earned increases over time.

• Doing credit reviews only annually. Customer health changes faster than annual reviews can capture. Continuous monitoring is the standard now.

• Ignoring monitoring alerts because most don't matter. The false-positive rate on credit monitoring is real, but treating all alerts as noise is how teams miss the one that mattered.

• No documented intervention playbook. When a monitoring alert fires, who decides what to do? If the answer is "the credit manager when they get to it," intervention happens too slowly to prevent the write-off.

• Not pulling fresh credit reports when monitoring flags material change. Monitoring tells you something shifted. A fresh report tells you what.

Frequently Asked Questions

What's the most effective stage for preventing bad debt?

Credit screening at onboarding. Financial Models Lab research shows the gap between strong-control and weak-control B2B firms in write-off rates (0.5% vs 1.8% of revenue) traces almost entirely to onboarding discipline rather than collections automation. The customers you never extended terms to are the customers who can't generate write-offs.

How do I know if my B2B write-off rate is too high?

Industry benchmarks help. The Atradius 2025 Barometer puts global B2B write-offs at around 6% of invoices, with North America slightly lower at 5%. As a share of revenue, strong-control firms keep write-offs below 0.5%, average firms run 1 to 1.5%, and weak-control firms exceed 1.8%. A rising trend matters more than a single number.

Can I prevent write-offs without enterprise software?

Yes, partially. The core prevention workflow (structured credit application, screening, conservative limits, periodic review) is process discipline first and tooling second. Free public sources (state UCC search, Google News, LinkedIn) cover a lot of the monitoring work for small portfolios. Software adds scale, not the workflow itself.

How often should I review existing customer credit?

Exposure-weighted. Top exposures: quarterly formal review plus continuous monitoring in between. Mid-tier exposures: semi-annual. Long tail: annual. Any account that hits a monitoring trigger gets reviewed immediately regardless of schedule.

What signals should trigger intervention before a write-off?

Payment behavior drift (DBT extending by 5+ days for two consecutive months) is the most reliable trigger. Atradius research confirms payment behavior changes precede formal default by months. Other reliable triggers: leadership departures without named replacements, LinkedIn headcount drops above 10%, new UCC filings, and negative news mentions.

Does AR automation prevent write-offs or just speed up chasing?

Both, but mainly the latter. Resolve's analysis shows AR automation reduces write-offs by around 30% over manual baselines, mostly by preventing aging-driven write-offs on customers who would have paid if asked at the right time. It doesn't prevent insolvency-driven write-offs, which is what credit monitoring does.

Should I use trade credit insurance as a prevention tool?

Trade credit insurance is risk transfer, not prevention. It pays out after a covered default but doesn't reduce the underlying default rate. Useful as a layer on top of strong prevention. Misused as a substitute for prevention because it makes write-offs less painful but doesn't make them less frequent. Providers include Allianz Trade, Atradius, Coface, and Euler Hermes.

How does AI change bad debt prevention?

AI is most useful in two places. First, synthesizing across data sources (news, LinkedIn, payment behavior, financial data) to surface the customers that actually warrant human attention. Second, prioritizing intervention by ranking accounts by probability of default. AI doesn't replace the prevention funnel. It makes each stage more efficient.

Summary

• Bad debt prevention is a funnel: screening, limit setting, continuous monitoring, intervention, then collections. Write-off is what gets through despite all of this.

• The highest-leverage stages are at the top of the funnel. Strong screening and continuous monitoring prevent more bad debt than any collections automation.

• Strong-control B2B firms keep write-offs below 0.5% of revenue. Weak-control firms exceed 1.8%. The 3x gap is mostly about prevention discipline.