- Most B2B customers do not default overnight. Distressed companies typically show warning signs 6 to 18 months before they file, according to bankruptcy research and credit bureau analysis.

- The earliest signals are usually outside the credit report: LinkedIn headcount declines, leadership departures, news sentiment, and web traffic. Payment behavior changes come next. Public filings (liens, judgments, bankruptcy) come last.

- One warning sign is noise. Two simultaneous signs is signal. Three or more is a workout situation, with no new credit extended until things clarify.

- A 2026 monitoring stack catches contextual signals (people, news, web) plus traditional ones (DBT, public records, financials). The bureaus alone catch roughly 30% to 50% of distressed customers in time to act.

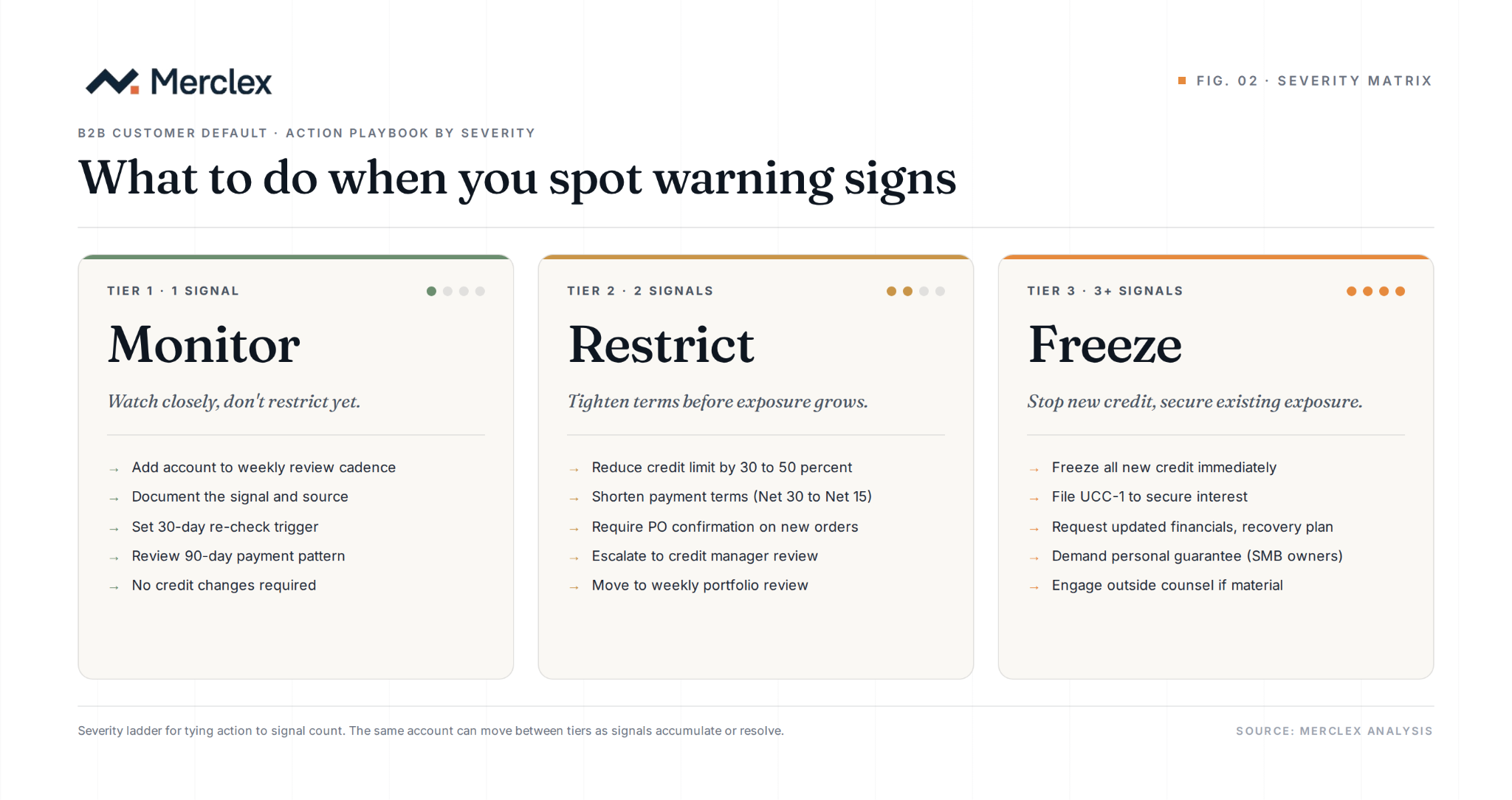

- he right action depends on the signal severity: monitor, restrict terms, or freeze the account.

How we built this guide

The framework below comes from Allianz Trade and Atradius insolvency research, NACM payment data, US Courts bankruptcy statistics, and direct evaluation of how operator-grade credit functions monitor risk in 2026. Operator playbook, not theoretical model.

How much warning do you actually get before a B2B customer defaults?

Most B2B customers do not default suddenly. According to research from Allianz Trade's economic insights team and bankruptcy practitioners, the typical company that files Chapter 11 was showing observable warning signs 6 to 18 months before the filing. The signals were there. They were not always read.

The most recent Atradius Payment Practices Barometer reports that bad debts now affect 6% of B2B invoices in Western Europe, and global insolvencies rose 19% in 2024 with another 5% rise forecast for 2025. The B2B environment is more fragile than it has been in over a decade. The companies that catch warning signs early lose less money than the companies that do not.

Three numbers frame the stakes. According to the National Association of Credit Management, 43% of US B2B credit sales are currently overdue. Bad debt write-offs run 1% to 4% of accounts receivable annually depending on industry. And US Courts data shows business bankruptcy filings in 2025 reached their highest level since 2014. The customers in your portfolio who will default in the next 18 months are already showing signs today.

How early do warning signs appear before a default?

Warning signs appear in a predictable sequence: contextual signals first (months 12 to 18 before default), payment behavior changes next (months 3 to 9), and public filings last (months 0 to 3). Operators who monitor only the credit report see the late signals. Operators who add contextual data see the early ones.

The earlier you can see the signal, the more options you have.

The pattern is consistent across Allianz Trade insolvency studies and academic research on financial distress. Companies cut headcount and lose CFOs before they stop paying invoices. They get sued before they file Chapter 11. The credit bureau is reporting on the past. The leading indicators are happening in real time on LinkedIn, in the news, and in your customer's communications.

What payment behavior signals predict B2B default?

The strongest payment-behavior predictor of default is a rising DBT (Days Beyond Terms) trend over multiple months, not a single late payment. A customer slipping from 5 days past terms to 25 days past terms over four quarters is paying its other vendors first and you second.

The five payment-behavior signals that actually predict B2B default:

- Rising DBT trend over four quarters. A single missed payment is noise. A trend of three consecutive months of rising DBT is signal. According to Atradius, the average US B2B payment runs 26 days past terms in 2025, up from prior years.

- Partial payments where full payments were the norm. A customer paying $50K against a $100K invoice with no dispute is preserving cash. They have other bills they cannot pay, and they are spreading the pain.

- Requests to extend payment windows or renegotiate terms. "Can we move from net 30 to net 60?" is a working capital ask. It is the customer's CFO telling you they cannot generate enough cash to cover terms as written.

- Sudden disputes on previously-uncontested invoices. A customer who has paid 24 invoices without question and is suddenly disputing the 25th is buying time. Disputes are the cleanest legitimate way to delay payment without admitting cash trouble.

- Bounced checks, failed ACH attempts, or last-minute remittance changes. Failed payments mean the customer's bank balance is too low to cover the invoice. This is usually the last signal before default.

These signals are necessary but not sufficient. By the time payment behavior is changing, the underlying distress has already been building for months. The earlier signals come from outside the AR ledger.

What observable business changes signal customer trouble?

The strongest non-payment predictor of B2B default is leadership turnover, especially in finance, followed by sustained headcount decline visible on LinkedIn. The Atradius Payment Practices Barometer consistently finds these are the strongest predictors of B2B default outside of payment behavior itself.

The seven observable business changes that warrant a re-pull and a conversation:

- CFO or COO departure without announced replacement. A CFO leaving in good times typically has a successor announced within 30 days. A CFO leaving with no replacement on the org chart 60 days later is a distress signal. Same applies to controllers and treasurers.

- Back-to-back exits in finance, ops, or sales leadership. One leadership exit is normal turnover. Three exits in 90 days from the same function is a sign the company is in trouble or about to be.

- 15%+ headcount decline on LinkedIn over 60 days. LinkedIn Workforce Reports and Workforce Intelligence tools have made this measurable in real time. The bureaus catch headcount declines six months later, if at all.

- Office or facility closures. Public lease terminations, "we are consolidating to one location" announcements, or visible closures of regional offices are usually cost-cutting under duress, not strategic optimization.

- Public layoff announcements via WARN Act notices. WARN Act filings are public, easy to track, and a definitive signal that a US company with 100+ employees is shedding workforce.

- Sustained service degradation on customer-facing operations. Slower response times, longer fulfillment, broken self-service portals. When companies cut people, the work that is left does not get done as well.

- Missed earnings or product launches for public customers. Analyst downgrades, missed quarters, or repeatedly delayed product launches are the public-company analog to private-company headcount cuts.

The unifying theme: companies that are in trouble cut humans before they cut invoices. If you only watch the AR ledger, you are reading the tail end of a story that started months earlier on LinkedIn, in WARN filings, and in the news.

What external events should make you tighten credit?

The strongest external triggers for tightening credit on an existing customer are industry-wide distress, the customer's own largest customer entering distress, and credit rating downgrades for public customers. These are forces from outside the customer that change their probability of default.

The four external events that change a customer's risk profile overnight:

- Industry-wide shocks. Commercial real estate in 2025, hospitality in 2020, trucking in 2023. When the customer's industry enters distress, individual customers become correlated. Allianz Trade country and sector risk reports track this systematically.

- The customer's largest customer entering distress. If your customer's largest customer is in trouble, your customer is next. Concentration risk stacks. This is one of the most overlooked early signals in B2B because most credit functions monitor their own customers but not their customers' customers.

- Credit rating downgrades for public customers. S&P, Moody's, and Fitch downgrades are public, time-stamped, and consequential. A downgrade from BB to B+ is a 50% increase in implied default probability over a five-year horizon.

- Major lawsuits, regulatory actions, or recall announcements. A class-action filing, an SEC enforcement action, or a product recall can take a solvent customer to insolvent in 90 days when the legal liability is large enough. PACER federal court filings are public.

External events do not always result in default, but they always justify a re-pull and a conversation. A customer with no internal warning signs but heavy external exposure should be on a tighter monitoring cadence than a customer with neither.

How do you systematically spot warning signs in 2026?

Spotting warning signs systematically in 2026 means combining three data layers in real time: traditional bureau data (DBT, public records, financials), payment behavior from your own AR system, and contextual signals from outside the credit report. No single layer catches everything.

The 2026 monitoring stack:

- Layer 1: Bureau data. Dun & Bradstreet, Experian Business, Equifax Business, or Creditsafe for trade payment data, public records, and risk scores. Refreshed monthly at best, often quarterly.

- Layer 2: Your own AR data. DBT trends, partial payments, dispute frequency, dunning response rates, requests to renegotiate. This is the data the bureaus do not have unless you contribute it. Modern credit intelligence tools integrate directly with QuickBooks, Sage, and NetSuite to pull this automatically.

- Layer 3: Contextual signals. LinkedIn headcount, leadership changes, news sentiment, web traffic patterns, review sentiment, WARN filings, court records. The leading indicators that show up months before the bureaus catch them.

A 2015 credit function had Layer 1 only. A 2020 credit function added Layer 2 in spreadsheets. A 2026 credit function combines all three with AI-prioritized alerts, so the team's time goes to investigating the 5% of alerts that move a decision rather than reading the 95% that do not.

What should you do when you spot a warning sign?

The right action depends on the severity of the signal: one signal warrants monitoring, two simultaneous signals warrant restricting terms, and three or more simultaneous signals warrant freezing the account.

Three tiers of response:

Tier 1: Monitor (one signal). Re-pull the credit report. Add the customer to a watchlist for weekly review. Document the signal and the date in the customer file. Reach out to the sales rep or account manager for context. Do not change terms yet. A single signal is often noise, and over-reacting on one data point creates relationship damage.

Tier 2: Restrict (two simultaneous signals). Reduce the credit limit by 30% to 50%. Shorten the payment window by one tier (net 60 to net 30, or net 30 to net 15). Require a deposit on the next purchase order. Document the decision and the data behind it. Communicate the change in writing.

Tier 3: Freeze (three or more simultaneous signals). No new credit extended until the situation clarifies. Switch new orders to cash on delivery or prepayment. Notify the sales team. Escalate to credit committee or finance leadership. Engage outside counsel if exposure is material. Begin the workout playbook: contact the customer to discuss the situation, request updated financials, and consider partial payment plans on existing balances.

The key principle: action scales with signal density, not signal type. Three medium-severity signals add up to a high-severity situation. One severe signal in isolation usually does not.

Frequently asked questions about B2B default warning signs

How early can you spot a B2B customer is going to default?

Distressed B2B customers typically show observable warning signs 6 to 18 months before they file for bankruptcy or default on payments, according to Allianz Trade research and bankruptcy practitioner data. The earliest signals are usually outside the credit report: leadership exits, headcount declines, and news events. Payment behavior changes come 3 to 9 months out. Public filings come last.

What is the strongest single warning sign of B2B default?

A rising DBT (Days Beyond Terms) trend over multiple months is the strongest single payment-behavior signal. Outside of payment behavior, the strongest signal is CFO or senior finance leadership turnover without an announced replacement, especially when paired with measurable headcount decline.

How many warning signs justify cutting off a customer?

A common operator rule: one warning sign warrants monitoring, two simultaneous signals warrant restricting terms (lower credit limit, shorter payment window, deposit required), and three or more simultaneous signals warrant freezing the account and switching to cash on delivery. Action scales with signal density.

Can you spot warning signs without buying a credit monitoring service?

Yes, partially. Free public sources cover several of the strongest signals: LinkedIn for headcount and leadership tracking, PACER for federal court filings, SEC EDGAR for public-company filings, WARN Act databases for layoffs, Google News for news sentiment, and your own ERP for payment behavior. What you cannot get for free at scale is automated alerting across your full customer portfolio, which is what modern credit intelligence platforms add.

What should you do if a customer becomes a workout situation?

A workout means the customer is materially impaired but not yet bankrupt. The standard playbook: freeze new credit, request updated financials and a recovery plan, consider taking a personal guarantee from owners of small businesses, file a UCC-1 to take a security interest where possible, and negotiate partial payment plans on existing balances. Engage outside counsel if exposure is material. Trade credit insurance carriers (if you have coverage) need to be notified within their claims windows.