• QuickBooks and Xero handle invoice creation, basic payment reminders, and AR aging reports. That covers a small B2B customer base where most people pay reliably.

• They do not support multi-step dunning sequences, credit onboarding with fraud checks, continuous customer risk monitoring, dispute tracking, collection agency forwarding, or behavioral reputation scoring.

• For businesses with more than 20 active credit customers, or with recurring late-payment problems, those gaps translate directly into higher DSO and avoidable write-offs.

• The standard approach is to connect a dedicated AR platform to QuickBooks or Xero rather than replacing either. The accounting tool handles the ledger. The AR platform handles the collection cycle.

Direct Answer

QuickBooks and Xero can handle B2B accounts receivable on their own when the customer base is small and reliably prompt. They generate and send invoices, send a single payment reminder, produce an AR aging report, and sync to the general ledger. For a business with 10 or 15 customers on net terms who mostly pay on time, that is often sufficient.

The gaps open up as the customer base grows, payment behavior becomes less predictable, or the finance team starts spending meaningful time chasing. Multi-step dunning sequences, credit decisions backed by actual data, monitoring for customer deterioration, dispute resolution workflows, and collection escalation: none of these are in QuickBooks or Xero. They are in dedicated AR software that connects on top of both platforms.

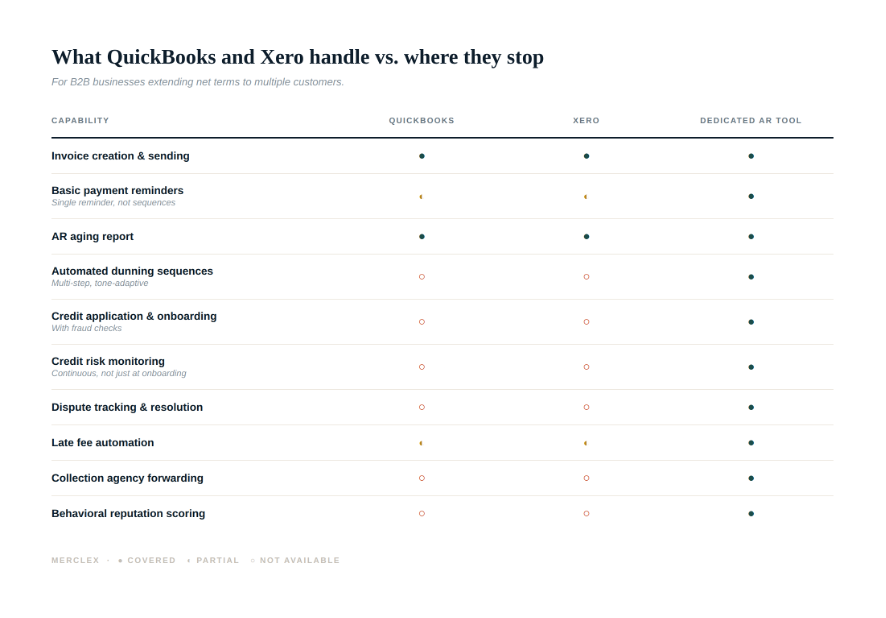

What QuickBooks and Xero Cover vs. Where They Stop

Ten B2B AR capabilities mapped across QuickBooks, Xero, and dedicated AR tools.

What They Handle Well

Invoice creation and delivery

Both platforms generate invoices from completed transactions, apply the right tax treatment, and send them to customers by email. QuickBooks has a more developed invoice customization system. Xero's interface is cleaner and its API is more widely connected to third-party tools. Either one handles this part of the job adequately.

AR aging reports

QuickBooks and Xero both produce AR aging reports showing what is outstanding, grouped by time bucket (current, 1-30 days, 31-60, 61-90, over 90). These are accurate and useful for reviewing the portfolio at a point in time. They are a lagging indicator: they show you what has already happened, not what is about to happen.

Basic payment reminders

Both platforms can send a payment reminder. QuickBooks allows a single automated overdue reminder at a configurable number of days past the due date. Xero's reminder system is similar. For a customer base where most people pay on time and a single nudge handles the rest, this covers the job.

Where They Stop

Multi-step dunning sequences

A dunning sequence is a series of timed reminders sent before and after the due date, with escalating tone and frequency for accounts that do not respond. QuickBooks and Xero send one reminder. A dedicated AR tool sends five, automatically, calibrated to the customer's payment history. That distinction alone explains most of the DSO difference between businesses using just an accounting tool and businesses using a dedicated AR platform.

Credit onboarding and fraud checks

When a new customer requests net terms, QuickBooks and Xero have no workflow for evaluating that request. There is no credit application, no EIN verification, no OFAC or sanctions check, no domain reputation check, no financial data review. The decision happens outside the system, usually informally.

A dedicated AR platform with credit onboarding handles this inline. The customer fills out a digital credit application. The platform runs automated checks in the background. The credit manager reviews a summary and sets terms. The whole process takes minutes rather than days, and the paper trail exists if the relationship ever goes bad.

Continuous credit monitoring

Even if a customer passes a credit check at onboarding, their financial health can change. QuickBooks and Xero have no mechanism to alert you if a customer starts showing signs of distress after you have extended terms: a news story about layoffs, a sudden drop in headcount, an earnings call with a revenue miss, a change in their payment behavior pattern.

Modern AR platforms monitor these signals continuously across the customer portfolio and surface accounts that are deteriorating before they miss a payment. That early warning is often the difference between a renegotiated payment plan and a write-off.

Dispute tracking and resolution

When a customer disputes an invoice, whether they are claiming a delivery issue, a pricing disagreement, or a quality problem, that dispute needs to live somewhere. In a QuickBooks or Xero-only environment, it typically lives in an email thread or a sticky note. A dedicated AR platform logs the dispute, links it to the invoice, tracks the resolution, and prevents duplicate reminders going out to a customer who is actively disputing a charge.

Collection agency forwarding

When a customer stops responding entirely, the last step before writing off is forwarding the account to a collection agency. In QuickBooks or Xero, preparing that handoff means pulling the customer record, exporting invoice history, attaching the contract, and sending a package manually. A dedicated AR platform does this in one click, with the contract, customer information, and invoice history already packaged.

Behavioral reputation scoring

Over time, a customer's payment behavior tells a story. Some customers always pay on day 35 regardless of the terms. Others pay promptly for six months and then start slipping. Others dispute every third invoice. A dedicated AR platform tracks this behavior over time, builds a reputation score for each customer, and uses it to calibrate both reminder sequences and future credit decisions. QuickBooks and Xero have no equivalent.

When QuickBooks or Xero Is Enough

Be honest about this. QuickBooks and Xero are genuinely sufficient when:

• The B2B customer base on net terms is small, roughly under 20 accounts.

• Most customers pay consistently within terms with minimal chasing required.

• There is no history of significant late payments or write-offs.

• Someone on the team has time to review AR aging weekly and follow up manually on anything outstanding.

At that scale, adding a dedicated AR platform creates work to set it up and maintain it that may not be justified by the problem it solves.

When You Need More

The indicators that QuickBooks or Xero is no longer enough:

• DSO consistently exceeds payment terms by 10 or more days.

• The same customers are late every cycle and follow-up is repetitive and manual.

• Credit decisions are being made without a formal process, and a write-off has come as a surprise.

• The AR function is taking more than a few hours per week of someone's time on manual tasks.

• The business is growing and the number of credit customers is outpacing the team's ability to manage them manually.

How the Integration Works

Dedicated AR platforms do not replace QuickBooks or Xero. They connect to them. The accounting tool remains the system of record for the general ledger, tax treatment, and financial reporting. The AR platform syncs customer records, open invoices, and payment status from the accounting tool, then handles all the collection workflow on top.

When a payment is received and matched in the AR platform, it syncs back to QuickBooks or Xero automatically. The finance team works in the AR platform for collection activity and in the accounting tool for everything else. The two systems stay in sync without manual data entry between them.

Frequently Asked Questions

Does QuickBooks have AR automation?

QuickBooks has basic invoice automation and a single automated overdue reminder. It does not have multi-step dunning sequences, credit onboarding tools, continuous customer risk monitoring, dispute tracking, or collection agency forwarding. Those capabilities require a dedicated AR platform that connects to QuickBooks.

Does Xero have AR automation?

Xero's AR capabilities are similar to QuickBooks: strong invoicing, a basic payment reminder, and AR aging reports. It does not support automated dunning sequences, credit checks, behavioral monitoring, or collection escalation workflows. Xero's open API makes it easy to connect dedicated AR tools, which is the standard approach.

What AR software works with QuickBooks?

Several dedicated AR platforms integrate natively with QuickBooks: Merclex, Chaser, BILL, InvoiceSherpa, and Quadient AR among others. The right choice depends on the size of your customer base, whether you need credit monitoring alongside collections, and your budget. Merclex covers credit onboarding, monitoring, and collections in one platform.

What AR software works with Xero?

Xero has a large third-party app ecosystem. Merclex, Chaser, Quadient AR, and BILL all connect to Xero. As with QuickBooks integrations, the choice depends on what capability gap you are filling: pure collections automation, credit risk monitoring, or both.

How much does AR software cost compared to just using QuickBooks or Xero?

Entry-level AR platforms start at $49 per month (InvoiceSherpa) and free tiers exist (Merclex). Mid-market platforms run $800 to $2,000 per month and above. The comparison is not the software cost versus zero: it is the software cost versus the time currently spent on manual AR work plus any write-offs that better monitoring would have prevented. For most businesses with a recurring late-payment problem, the math resolves within the first month or two. See merclex.com for current pricing.

Can you use QuickBooks for credit risk management?

No. QuickBooks records payment history for existing customers, which is useful context, but it has no tools for evaluating new customers before extending credit, no automated fraud checks, and no system for monitoring customers continuously after credit is extended. Credit risk management requires a dedicated platform or a credit bureau integration.