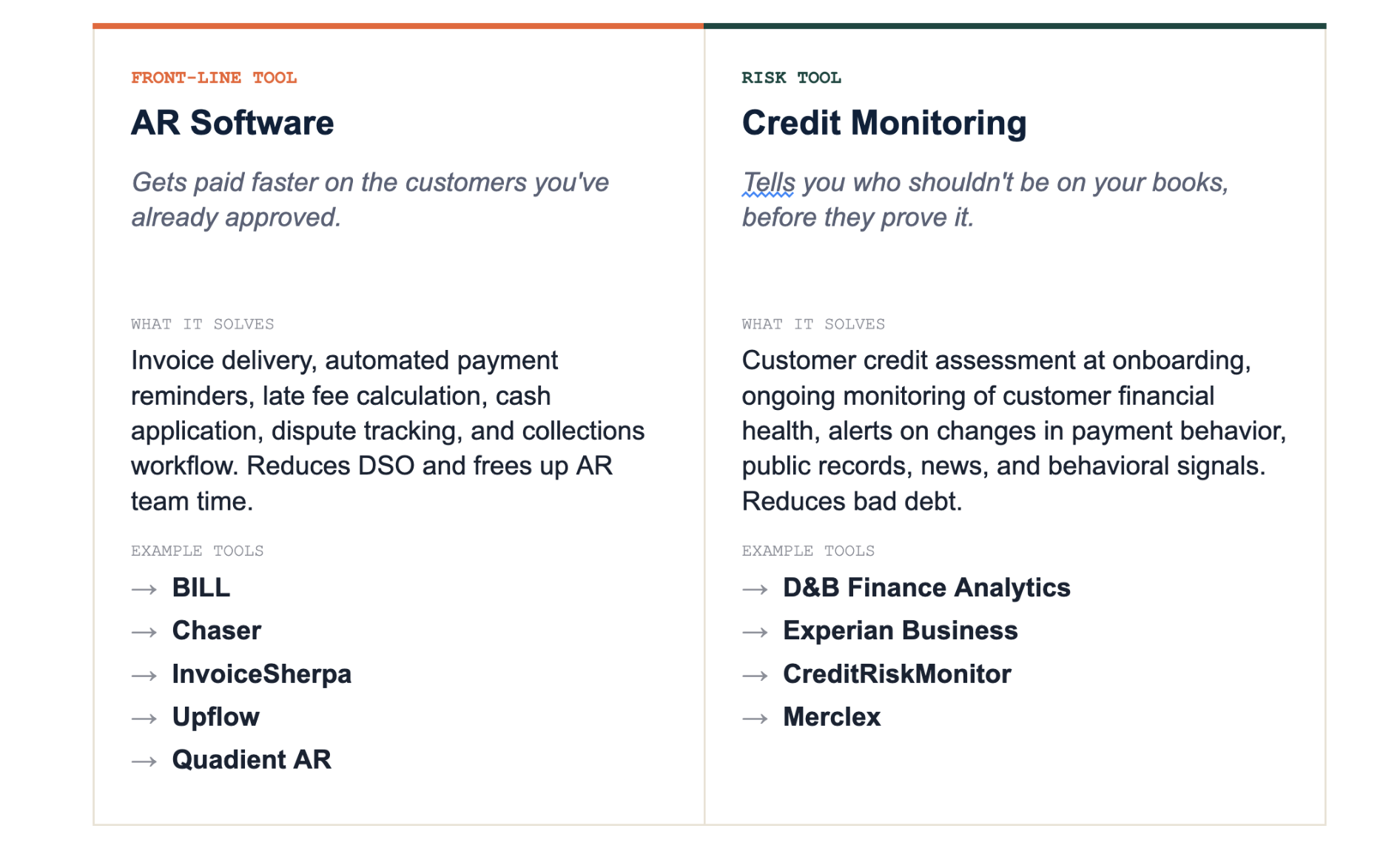

• AR software and credit monitoring platforms solve different problems. AR software collects what you're owed. Credit monitoring tells you who shouldn't be on your books in the first place.

• Most B2B finance teams that extend credit on net terms need both. The two work together: monitoring prevents the bad debt that AR software then doesn't have to chase.

• If you only have budget for one, pick based on your actual pain. If write-offs and bad debt are the issue, monitoring. If late payments and slow cash flow are the issue, AR software.

• Some platforms combine both. Merclex, Bectran, and HighRadius (at the enterprise end) all offer integrated AR plus credit risk in a single workflow.

Direct Answer

AR software automates the post-sale collection workflow: invoice delivery, payment reminders, late fees, dispute tracking, cash application. Its job is to collect what you're owed faster and with less manual work. Tools like BILL, Chaser, InvoiceSherpa, and Upflow live here.

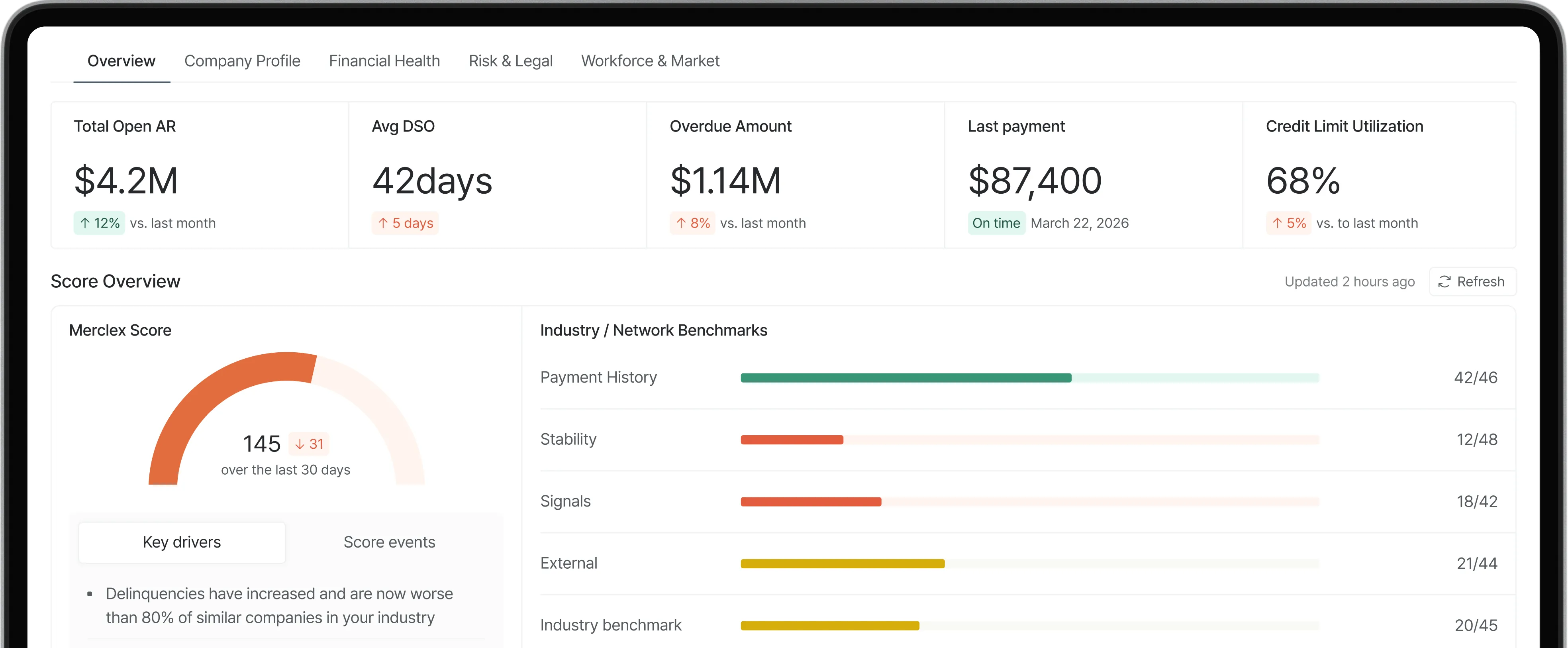

Credit monitoring platforms work on the front and the middle of the credit cycle. They assess whether a customer should be extended credit at onboarding, and they continuously watch existing customers for signs of deterioration. Tools like D&B, Experian, CreditRiskMonitor, and Merclex live here.

The honest framing: these are complementary tools, not alternatives. AR software helps you get paid faster on customers who can and will pay. Credit monitoring helps you avoid the customers who can't or won't. Most B2B finance teams that extend net terms benefit from both.

A Tale of Two Tools

Here's the side-by-side, with example platforms in each category.

Key Definitions

• AR software (accounts receivable automation): Tools that handle the workflow after a sale has been made, from invoice to cash. Doesn't make credit decisions.

• Credit monitoring platform: Tools that assess and track the creditworthiness of your customers, both at onboarding and continuously.

• Days Sales Outstanding (DSO): The average number of days it takes to collect payment. AR software targets this metric.

• Bad debt / write-offs: Invoices that are never collected. Credit monitoring targets this metric.

• Integrated platforms: Tools that combine both AR and credit monitoring in one product. Merclex, Bectran, and HighRadius are examples.

Which One Do You Actually Need?

Use this rough rubric. The right answer for most B2B finance teams is "both," but the path to that depends on what's hurting you today.

Common Mistakes

• Buying AR software to solve a credit problem. Automated reminders sent more frequently don't make insolvent customers pay. If your write-offs are rising, AR software alone won't fix it.

• Buying credit monitoring to solve an AR problem. A dashboard full of risk signals doesn't reduce DSO if the underlying issue is manual chasing. Wrong tool for the symptom.

• Assuming the same vendor handles both well. Many vendors market both products. The quality varies. Evaluate each module independently rather than trusting the bundle.

• Treating one tool as a substitute for the other. They overlap on data inputs (AR aging informs both) but they target fundamentally different outcomes.

• Putting off the second tool indefinitely. Teams pick one, get partial relief, and live with the other problem for years. The cost of the unaddressed side compounds quietly.

Frequently Asked Questions

Can AR software replace credit monitoring?

No. AR software is built to collect on invoices that already exist. It has no model for whether the customer who created those invoices is heading toward default. The two tools answer different questions: "How fast will I get paid?" versus "Will I get paid at all?"

Can credit monitoring replace AR software?

Not for most teams. Credit monitoring tells you who to watch and who to act on. It doesn't send invoices, calculate late fees, or run dunning sequences. Some integrated platforms (Merclex, Bectran) include both, but a pure credit monitoring tool won't replace AR automation.

Which one should I buy first if I can only afford one?

Diagnose the pain. If bad debt and write-offs are bleeding cash, buy monitoring first. If late payments and AR backlog are the issue, buy AR software first. The biggest mistake is buying based on which is more familiar or more heavily marketed, rather than which solves your actual problem.

Do any platforms do both well?

A few. Merclex was built specifically to combine credit risk monitoring with AR workflow for B2B trade businesses. Bectran offers both for distributors and mid-market. HighRadius does both at the enterprise tier. Most legacy bureaus and most AR-only vendors don't combine the two effectively.

How much should I expect to spend on each?

AR software under $500 a month covers SMB to lower mid-market. Credit monitoring at the same tier exists (Experian Business CreditScore Pro at $124/mo, Merclex free starter, D&B Credit Reporter from ~$100/mo). Enterprise-grade either way runs $10K+/year. The combined cost of both at SMB tier is usually less than one enterprise contract.

Does my ERP already include either of these?

Most ERPs include basic AR functionality (invoice creation, AR aging reports) but limited automation. Credit monitoring is rarely native to ERPs and almost always requires a separate tool or add-on. Check what your ERP actually does before assuming you have either capability.

Summary

• AR software collects faster. Credit monitoring prevents the wrong customers from getting on your books to begin with.

• Most B2B trade teams need both. A few integrated platforms (Merclex, Bectran) combine them.

• Pick based on your pain, not on what's more familiar. Write-offs need monitoring. Slow payments need AR software.